Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

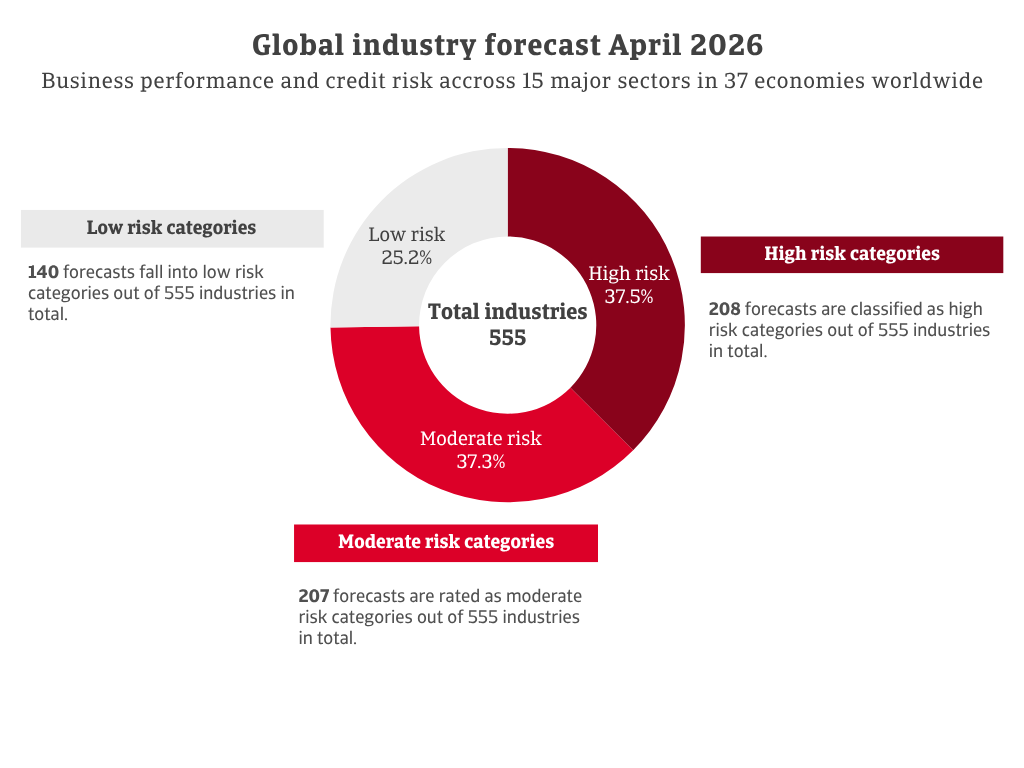

We have released an updated industry forecast per market for Q2 of 2026, providing business performance and credit risk assessments from our underwriters. The chart covers key sectors across representative markets in Europe, the Americas, and Asia-Pacific, reflecting global economic activity.

In total, 555 forecasts have been issued. Of these, 140 fall into low-risk categories, 207 are rated as moderate risk, and 208 fall into the high-risk category. This represents an increase of 14 sectors in the high-risk group since January 2026. The chemicals sector is the most affected by recent downgrades, with conditions worsening most sharply in Europe. This outcome is unsurprising, given the sector’s strong exposure to sharp oil and gas price volatility driven by the war in the Gulf.

Forecasts for food, pharmaceuticals, financial services, chemicals, electronics/ICT, and agriculture are more favourable than the overall benchmark. Machines/engineering and services remain at mid-range risk levels. Transport, automotive, consumer durables, and paper show elevated risk. The most negative outlook is concentrated in construction, metals/steel, and textiles.

High oil and gas prices weigh on the sector, while competition remains intense with producers from Europe and overseas. Belgian chemical production is forecast to fall by 2.5% in 2026. Payment delays have increased in recent months.

Revenues across Belgian machinery firms continue to decline, and non-payments are rising. Output fell by 10.8% in 2024 and by a further 2.3% in 2025.

The services sector benefits from higher prices and stronger revenues. At the same time, non-payments have declined, supporting a more stable outlook.

The sector suffers from increased volatility of oil and fuel prices due to the war in the Gulf. Smaller transport and logistics firms feel the greatest pressure, especially sole proprietorships. These operators typically have limited bargaining power and long pricing agreements.

Credit risk worsened in the second half of 2025 as credit insurance claims increased. The agri-food trade balance fell to EUR 0.2 billion in 2025, down from EUR 4.4 billion in 2024. This decline reflects the sector’s weakening competitiveness.

Credit insurance claims rose during the second half of 2025, accelerating in the fourth quarter. After contractions in 2024 and 2025, production is expected to fall by 0.9% this year. Order books remain weak outside strategic sectors.

Market conditions remain challenging. In 2025, bankruptcies rose by 7% in B2B services and by 5% in B2C. Credit insurance claims remain high.

Insolvencies declined slightly last year, but conditions in goods transport remain difficult. Rising costs continue to strain liquidity, although the air transport segment remains relatively resilient.

Production is forecast to rebound by 2.5% this year after sharp falls in 2024 (-19.8%) and 2025 (-7.9%). Weak consumer spending and high energy prices suppress demand for cars. Production relocations further weaken the short-term outlook.

Chemical production is expected to fall by 4.6% this year. High oil and gas prices are raising costs, while cheap Chinese chemical goods intensify competitive pressure in international markets. US tariffs are also weighing on performance.

Rising input prices have dampened activity once again. Credit risk remains high due to unstable demand, liquidity shortages, cautious bank lending, and long payment times. Small and medium-sized enterprises face intense competition, margin pressure, and liquidity issues.

After modest results in 2024 and 2025, output is expected to decline by 1.6% this year. Rising energy costs are driving inflation and reducing real incomes. Private consumption in Italy is expected to stall in the second quarter and average just 0.4% in 2026.

The sector was downgraded in the first quarter of 2026 due to weak output and limited investment in modernisation. Higher oil and gas prices linked to the Gulf war have prompted a further downgrade. Plant closures and divestments continue, while falling earnings and high debt have increased credit risk.

Construction output is expected to grow by 1.3% this year. Residential activity is accelerating, with completed homes forecast to rise from 68,000 in 2025 to 80,000 in 2026 and 84,000 next year. Competition keeps margins low, but most firms remain profitable.

Weaker firms have exited the market in recent years, while remaining businesses have shown steadier performance since the pandemic. Even so, credit risk remains elevated.

The sector faces growing challenges, including tariff risks and weaker international competitiveness. Domestic pharma production is decreasing. More firms are investing in the US and China, slowing domestic innovation projects and clinical trials. Credit insurance claims have also risen compared with historical levels.

The chemicals sector is technology led, with strong specialist niches, but remains exposed to economic cycles and complex regulation. Recent jumps in oil and gas prices are expected to weigh on production.

Sales are forecast to rise by 1.8% after a 4.4% fall last year. Demand depends heavily on household confidence and interest rates. Volatile demand, margin pressure, and inventory risks remain long-term challenges.

The sector is expected to grow by 4.7% this year after a 6.7% contraction in 2025. It remains globally competitive, with strong technical expertise and diversified demand across industry and infrastructure.

Services remain diverse and are forecast to grow by 2% in 2026. B2B and essential services show relative stability, while consumer-focused segments remain sensitive to economic swings.

After declines in 2024 and 2025, production is forecast to rebound by 3.1% in 2026. However, competition remains fierce, cost-pressure is high. Pricing power is weak and exposure to weak retail demand persists.

Chemical production is forecast to fall by 5.1% in 2026, following a 6.4% decline in 2025. High domestic energy costs weigh on competitiveness, while cheaper imports erode margins. The Gulf war is also raising input costs and disrupting raw material supply.

By 2026, climate-related risks such as floods and droughts have become structural. In stressed scenarios, they can increase expected losses by 60% to 100%. Weather events, including the Sumatra floods, have shifted from occasional disruptions to long-term threats. This uncertainty has driven the downgrade.

Non-payments have increased, particularly in the meat and fish segments. Market oversupply is straining liquidity among food importers.

Rising living costs, persistent inflation, and intense competition continue to challenge firms. Business closures are increasing, especially in food and beverage. Non-payments have risen in both sectors, and this trend is expected to continue.

Overall performance remains solid, but non-payments have increased compared with earlier periods, leading to higher credit risk.

The war in the Gulf has caused widespread disruption across the region, including the UAE. The UAE economy is now expected to grow by just 0.3% in 2026, down from a 4.8% forecast in February.

Growth in the non-oil economy is expected to slow to 0.7% this year, compared with the 5.2% forecast earlier. Trade disruption and uncertain demand have weakened manufacturing. At the same time, higher costs, tighter financing, and weaker confidence linked to the conflict are weighing on construction. The services sector, which depends heavily on tourism, consumer footfall, and positive sentiment, is expected to contract by 0.9% this year. Banks and financial firms remain stable for now.

The UAE relies on the Strait of Hormuz for its exports, which limits its ability to benefit fully from higher oil prices. Storage constraints will also restrict production. As a result, oil activity is expected to fall by 1.2% this year. Trade constraints will continue to weigh on the wider economy.

As a result, most major sectors in the UAE have been downgraded:

The Atradius industries forecast per market is a global chart that provides an expert view of business performance and credit risk across different sectors and markets. It covers 15 major industries in 37 representative economies. Each sector-market combination is assigned an opinion - excellent, good, fair, poor, or bleak - based on the insights of Atradius’ specialised risk analysts.

These underwriters work from centres of expertise around the world, ensuring that every assessment reflects local realities and is informed by on-the-ground knowledge. This approach highlights the strength of Atradius’ risk management system and its ability to anticipate challenges in global trade.

Important note: While the chart offers a powerful overview, it is important to remember that risk does not reside in countries or sectors but in individual buyers. That is the true value of credit insurance: the ability of our underwriters to deliver a guaranteed, near-instant opinion on virtually any buyer worldwide, enabling businesses to trade with confidence.

To explore to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.