Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

As we move towards the close of the year, it is the right time to reflect on how businesses around the world have navigated B2B payment risks in the current fast-changing and often unpredictable economic and trading environment.

This year’s edition of our global survey on business-to-business (B2B) payment behaviour – the Atradius Payment Practices Barometer – offers a detailed view of how companies across various markets and industries navigate economic uncertainty, shifting customer payment behaviour and rising insolvency risks. Survey findings reveal just how challenging it has become for businesses to operate under these conditions. Many are feeling the strain, particularly when faced with changes in B2B payment behaviour that leave them more exposed to risk.

Based on feedback from 7,500 businesses across 35 markets, the survey provides a direct window into payment practices in Western Europe, Central and Eastern Europe, North America, Asia, Australia and the United Arab Emirates (UAE). These insights matter because they come straight from businesses themselves, those managing the day-to-day realities of trade, credit and cash flow.

To understand how exposed businesses are to B2B payment risk, our survey focuses on three key indicators: the share of overdue invoices, which shows how widespread payment delays are; Days Sales Outstanding (DSO), which tracks how quickly companies convert invoices into cash; and bad debt write-offs, which reflect actual financial losses from unpaid invoices. The first two act as early warning signs, flagging shifts in payment behaviour that could lead to future losses. Write-offs confirm that the risk has materialised, directly affecting profitability.

This year’s results paint a mixed picture. While some regions have seen a slight decline in overdue invoices, progress remains modest. In Western Europe, for instance, 47% of B2B invoices are still paid late, with delays largely driven by financial stress across the economy. Bad debts now affect an average of 6% of B2B invoices, a clear sign that more businesses are struggling to recover what they are owed.

The situation is even more severe in markets like India, where overdue invoices affect 63% of B2B sales and bad debts have risen to 7%. Across the board, the most common reason for late payments remains customer cash flow pressure, followed by supply chain disruptions and internal inefficiencies. These challenges are particularly acute in Western Europe and North America, where 34% of businesses report delays linked to supply chain issues.

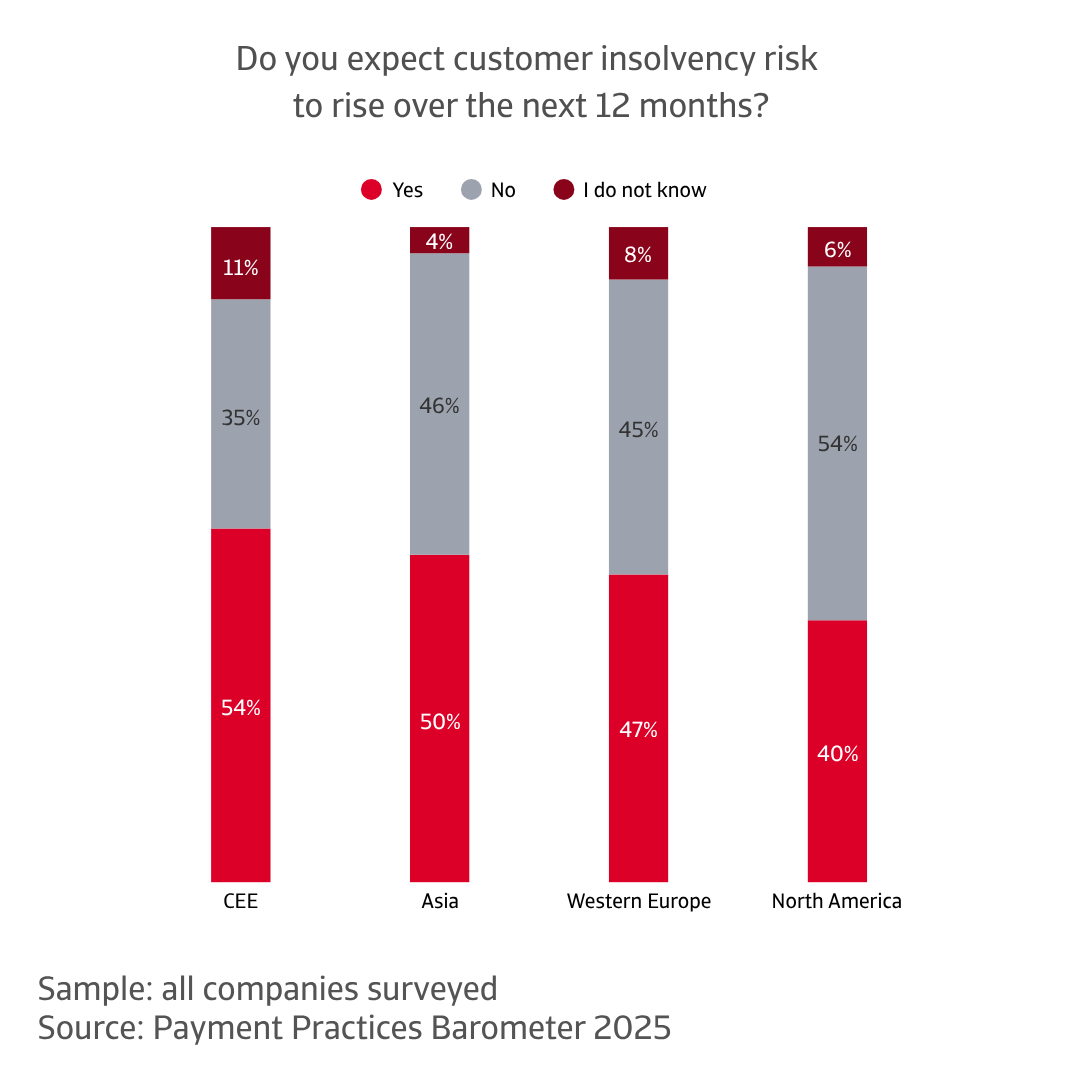

What’s clear is that businesses are operating in a more fragile environment. Many are strengthening credit management, but the risk of customer insolvency is rising. Nearly half of companies in Western Europe expect insolvencies to increase in the months ahead. This makes agile and proactive payment risk strategies more important than ever.

The regional landscape shows a complex mix of progress and persistent challenges. In Asia and North America, businesses surveyed appear to be freeing up liquidity from receivables more quickly than their counterparts in Europe. This suggests stronger progress in turning invoices into cash.

Western Europe has made some gains in cash collection, but these have yet to translate into significantly faster payments. In Central and Eastern Europe, payment speed is under pressure, driven by tighter working capital and increased borrowing needs. Write-offs, which reflect the final impact of payment risk, also show regional contrasts.

In North America and Western Europe, write-off rates show slight downward trend, a positive sign that points to gained efficiency in debt collection. In Asia, however, write-offs have increased despite faster cash collection, suggesting that customer credit quality is deteriorating. In Central and Eastern Europe, write-offs remain unchanged, highlighting persistent challenges in recovering bad debts. These may stem from weaker legal frameworks or less efficient collection processes.

These payment trends unfold against a backdrop of rising insolvencies, as the broader economic picture remains increasingly sobering. Global insolvencies are forecast to rise by 5% in 2025, following a sharp 19% increase in 2024. Although a slight decline of 3% is expected in 2026, the overall trend remains concerning. The surge in 2024 was driven by high input costs, elevated interest rates and the withdrawal of pandemic-era support measures.

The risk is not always visible in payment behaviour. Many businesses are paying faster, often under stricter credit terms imposed by suppliers. But this does not mean they are financially sound. In several markets, companies continue to struggle with high debt burdens, weak demand and rising operating costs. Some manage to pay on time but collapse shortly after. Others skip payment altogether, leading to write-offs and insolvency.

Early data from 2025 already exceed projections, suggesting that adverse conditions are proving more persistent than expected. Additional pressure is coming from higher tariffs and growing policy uncertainty, both of which are dampening global growth and discouraging investment. Against this backdrop, insolvency expectations vary significantly across regions, reflecting a mix of caution, concern and uncertainty.

In North America, the sentiment is largely cautious. Most companies do not expect insolvency levels to improve in the near term. The prevailing mood is one of watchfulness, with businesses preparing for stress that may not yet be visible on the surface. In Asia, more companies anticipate a rise in insolvencies than those expecting stability. Many are staying alert to potential external shocks and closely monitoring global developments that could affect their operations.

In Western Europe, expectations are more divided. Some businesses believe current conditions can hold, while others are bracing for deterioration, reflecting the region’s economic uncertainty. In Central and Eastern Europe, concern is more pronounced. Businesses in the region are particularly wary of a potential increase in insolvencies, given their exposure to global headwinds and the need for robust risk management.

Across all regions, one thing is clear: expectations are mixed, but businesses are watching, preparing and adapting.

Looking ahead to next year and beyond, the question is simple: what challenges do companies across markets and industries expect to face that could affect their financial health?

Across regions, the answers differ, but the underlying message is clear. Businesses are operating in a world where uncertainty has become the norm. In North America, companies remain alert to economic instability and unpredictable market shifts. While many feel confident in their ability to navigate these challenges, the mood remains cautious. Beneath the surface, there is an awareness that conditions could change quickly.

In Asia, the pressure is more acute. Businesses are highly exposed to global volatility and regulatory shifts, and their deep integration into global supply chains means that even minor disruptions can have disproportionate effects. Across all markets, insolvency levels are expected to remain elevated throughout 2026.

In Western Europe, the picture is more complex. No single issue dominates, but a combination of pressures—economic, political and structural—creates a fragile equilibrium. Businesses are managing this complexity with caution, aware that resilience now depends on agility and foresight. In Central and Eastern Europe, the concern centres on market unpredictability. Tight liquidity and rising borrowing needs are making payment cycles harder to manage, increasing the strain on financial stability. Businesses in the region are navigating a delicate balance, where access to finance and risk exposure must be constantly reassessed.

Across all regions, one theme stands out: resilience is no longer optional, it is essential. Companies are reassessing risk, strengthening credit management and seeking clarity in a business environment that offers little of it. In a world where uncertainty is the only constant, insight becomes a strategic advantage. With the right knowledge and strategic customer payment risk management, involving also insurance solutions, businesses can move forward with confidence, across borders, across sectors and across cycles.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Businesses across 35 markets report persistent challenges with overdue invoices, bad debt write-offs and slower cash conversion highlighting the fragility of today’s trading environment

Regional contrasts reveal uneven progress with modest gains in some markets and mounting pressure from tight liquidity, slower payments and persistent bad debt recovery challenges

Despite some improvements in payment speed, insolvency forecasts remain concerning with many businesses collapsing shortly after meeting payment terms

Companies are strengthening credit management and reassessing risk strategies to adapt to a world where uncertainty is constant and insight is a strategic advantage