Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

Selling on credit remains a defining feature of business-to-business (B2B) trade in the Netherlands. Nearly three quarters of B2B sales are made on credit, more than twenty percentage points above the Western European average. Far more companies in the Netherlands than in Western Europe set payment terms within a 30-day credit window and, on average, payments are collected three weeks after invoicing, as shown by Days Sales Outstanding (DSO). This efficient cash conversion cycle helps reduce the amount of working capital tied up in unpaid invoices and keeps credit losses contained, with bad debt write-offs hovering around 1% of B2B invoices market-wide.

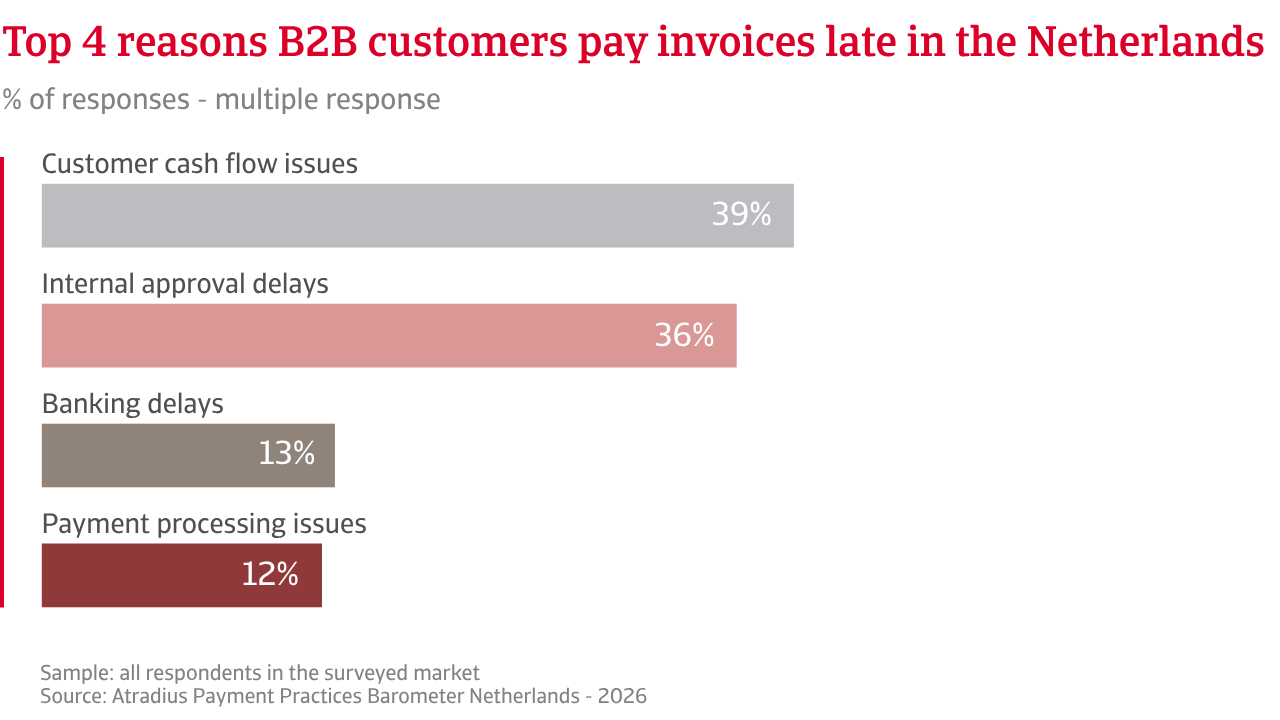

Beneath these figures, however, lies a broader pattern of late payments, which is widespread across the market. Seven in ten Dutch suppliers, a slightly lower share than in Western Europe, report delays from B2B customers. Just under one fifth of Dutch B2B invoices are past due, compared with nearly one quarter in Western Europe. Invoices often remain outstanding for two weeks beyond the due date. This is shorter than the three-week average in Western Europe, yet still long enough to create concentrated risk exposure. When input costs rise, growth slows, or borrowing becomes more expensive, customer liquidity tightens quickly. Many customers stretch payment timelines, shifting short-term financing needs upstream to suppliers. Nearly one third of Dutch suppliers now report cash flow pressures linked directly to customer liquidity strains.

Exposure to credit risk varies across sectors. Wholesale trade, SMEs and parts of the services sector are particularly affected because margins are tight and liquidity stretched. Even a small share of overdue invoices places pressure on cash flow, working capital and profitability. Many of these companies often face higher write-offs, sometimes above 5%, compared with the market average of one per cent of invoiced turnover. This shows payment risk in the Netherlands is widespread and concentrated in clusters of risks that can create disproportionate financial strain.

To mitigate these pressures, more Dutch companies than in the region maintain financial buffers, tying up capital that could support investment. They also make wide use of digital payment tools to encourage timely settlement, while more businesses in Western Europe than in the Netherlands request upfront payment from customers to mitigate credit risk. Western European and Dutch companies alike often combine internal credit control with outsourced credit risk management, including credit insurance. However, Dutch businesses in particular report that this mix of tools helps them manage unpredictable B2B payment behaviour more effectively in the current unsettled economic and trading environment.

Nearly three quarters of B2B sales are made on credit, more than 20 percentage points above the Western European average.

In line with expectations across Western Europe, a significant number of Dutch companies expect insolvencies to rise in the short term. They say this is likely to rise if economic growth stays modest, financing conditions remain tight, and geopolitical tensions continue to disrupt trade flows. Concern is strongest among export-oriented firms, where weaker global demand and uncertainty around global trade could quickly increase the risk of financial distress.

Our survey remained open long enough for respondents to factor in signs of shifting economic conditions and wider geopolitical tensions, giving Dutch businesses time to reflect on the possible consequences for profitability. This may explain why expectations are uneven, yet still more positive than across Western Europe, as Dutch firms show slightly greater confidence that margins can hold up in the short term even if the overall mood remains cautious.

Larger manufacturers appear more insulated, citing pricing power, diversified revenue streams and stronger balance sheets as reasons they do not anticipate major margin disruption. Other companies, particularly SMEs with high exposure to global markets, thinner margins, or limited financial reserves, expect to face ongoing fragility. For these firms, even modest shifts in economic conditions can have outsized consequences, which makes close cash-flow monitoring vital.

.2026-05-15-14-01-38.png)

Several factors are expected to shape B2B payment patterns in the short term. Dutch businesses echo Western European concerns that cost pressure linked to inflation will continue squeezing margins across many sectors, leaving firms with less financial space and greater sensitivity to payment delays. An economic slowdown would add further pressure due to softer demand, reducing turnover and increasing the likelihood that customers will postpone payments to preserve liquidity.

Regulatory change also plays a role. Adjustments to reporting rules and new compliance requirements can be challenging, particularly for smaller firms with constrained back-office capacity. Businesses say these changes absorb time that would otherwise support credit control. Sector-specific pressures further complicate the outlook. Industries under strain, like construction and transport, face cyclical swings and contract delays, which can translate directly into slower payments and tighter working capital conditions.

Looking ahead, Dutch B2B payment behaviour will be shaped increasingly by external economic and geopolitical forces. The high reliance on trade credit means any pressure on customer liquidity passes quickly up the supply chain. Firms told us they are focusing on careful internal credit control, supported by strategic credit risk tools, including insurance, to stay resilient in a more unsettled operating environment.

For a full overview of the 2026 survey results for the Netherlands and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.