Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

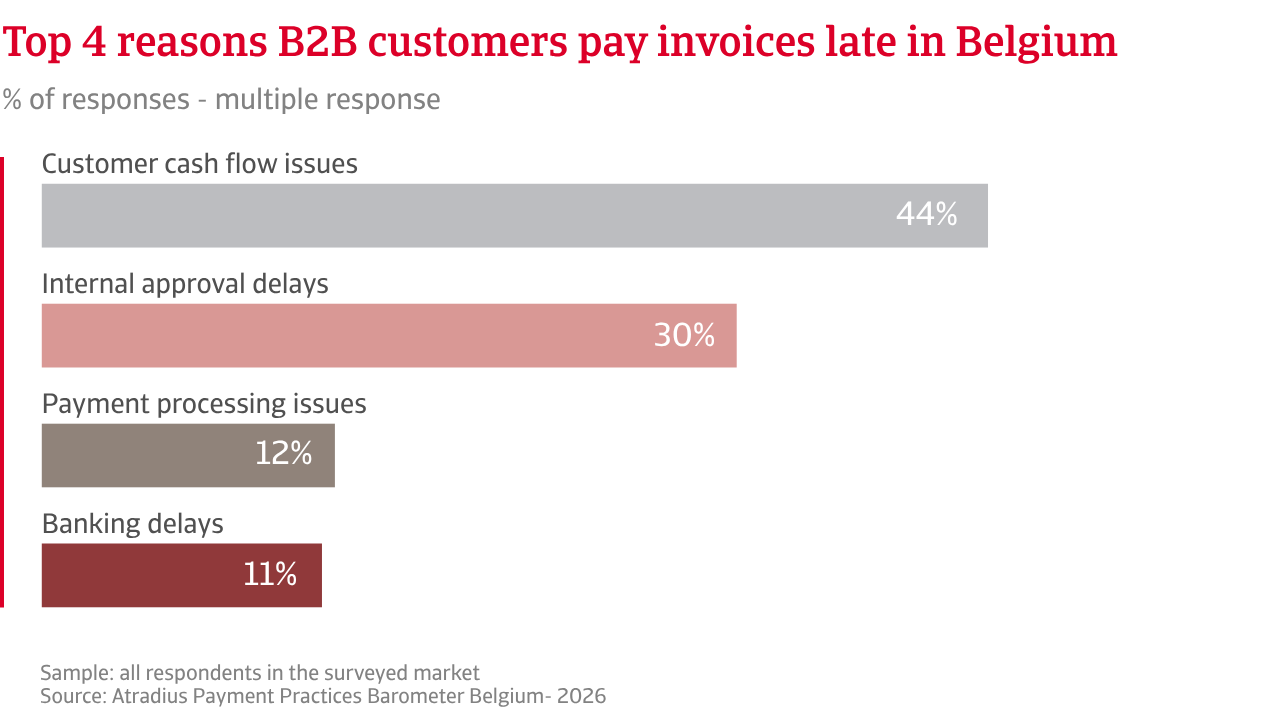

Pressure is growing on Belgium’s business-to-business (B2B) payment environment. Survey findings indicate that, in recent months, the trade credit risk landscape has become comparatively more fragile in Belgium than in much of Western Europe. 54% of B2B sales in Belgium are now made on credit, a slightly higher share than in Western Europe. This supports demand but increases suppliers’ exposure to customer payment risk in a tight liquidity environment. More companies in Belgium than in Western Europe set payment terms at 30 days from invoicing, which helps limit working capital exposure while maintaining trade relationships. Payments are collected on average slightly beyond this period, as reflected in the market-wide Days Sales Outstanding (DSO). This indicates that many companies, mainly SMEs in trade, continue extending payment terms to sustain business, which can increase exposure to payment risk.

Belgium’s economy has grown at a moderate pace in recent months. Business cash flow remains tight. Geopolitical turmoil and weak global demand add pressure, prompting businesses to hold cash longer and stretch payment timings. This has contributed to a clear deterioration in B2B payment behaviour in the market. 84% of Belgian suppliers, above the Western European share, now report delays from B2B customers. Past due invoices account for around 28% of invoiced B2B turnover, just above the one-quarter benchmark for Western Europe. Survey findings show that just over two in five companies in Belgium, broadly in line with the Western European benchmark, now rely on delayed payments to ease liquidity pressure. Construction and trade companies are the most likely to rely on this practice.

.2026-06-03-08-40-41.png)

Bad debt losses in Belgium have increased in recent months, driven mainly by customer insolvency, inactivity, or unreachability, particularly among SMEs in trade. Almost as many companies in Belgium as in Western Europe report contained losses of up to 1% of invoiced B2B turnover, and fewer report losses of up to 2% compared with the Western European benchmark. The picture shifts at higher loss levels, as almost twice as many businesses in Belgium as in Western Europe report bad debt losses of up to 5% and beyond. Higher loss levels erode working capital directly and reduce the financial capacity, particularly of SMEs already facing tight liquidity. Against this backdrop, one-third of companies report reduced cash available for operations and more than a quarter turn to external financing to bridge funding gaps.

Ongoing cash flow pressure from delayed payments, alongside collections extending beyond payment terms, is shaping credit risk management choices in Belgium. Survey findings show that Belgian companies place strong emphasis on credit insurance and active credit management to limit the impact of payment risk. This is complemented by greater use of secured payment terms than across Western Europe. Comparatively lower reliance on bad debt reserves suggests limited appetite to absorb losses internally. Together, these practices point to a clear preference for limiting exposure upfront rather than managing losses after they arise, particularly among SMEs and trade-exposed sectors.

As the year unfolds, Belgian businesses expect payment behaviour to deteriorate, with SMEs in trade and construction braced for rising customer payment risk amid tighter liquidity and slower settlement.

Belgium heads into the coming months with a weaker payment landscape than most of Western Europe. More companies expect B2B payment behaviour to deteriorate in the short-term than to improve, particularly among SMEs in trade and construction. These sectors anticipate an increase in customer payment risk and rising pressure on liquidity. Confidence in short-term profitability is also softening. While some businesses still expect margins to improve, the overall mood is much more muted. By contrast, sentiment across Western Europe is firmer, suggesting room for companies to protect their margins. The contrast reinforces the view that Belgium is moving into a more demanding phase of the cycle, with less headroom and greater sensitivity to cost pressure and slower settlement.

There is a clear difference in expectations about insolvency levels between Belgium and the rest of Western Europe. A larger share of Belgian companies anticipate insolvencies will rise, reflecting ongoing strain in parts of the economy where cash conversion is slowing. Construction is the most visible pressure point. Companies in this sector, along with those in trade, say the impact of customer payment risk is making day-to-day cash flow much harder to manage. Together, these two sectors sit at the centre of Belgium’s payment-risk scenario in the short-term. Businesses in Belgium anticipate a risk landscape broadly in line with that expected across Western Europe, though domestic factors heighten some pressures. Domestic economic growth is expected to remain modest, providing little relief for companies already operating with tight liquidity. Ongoing inflation-related cost pressures are expected to further constrain liquidity and increase payment delays.

.2026-05-15-14-50-52.png)

Fraud risk stands out as a growing concern. This is reported by a larger share of Belgian firms compared with many Western European peers and points to operational weaknesses across supply chains. Geopolitical instability is also cited as a major risk affecting B2B payment behaviour in the short-term. There is concern about global conflicts, supply chain disruptions, and uncertainty in international trade. Firms are particularly attentive to tensions in key export markets, energy supply risks, and the potential impact of sanctions or regulatory changes on cross-border operations. As risk expectations increase, around two in five Belgian companies say shifts in B2B payment outlook have pushed them to take a more structured approach to managing customer payment risk to keep short-term cash flow steady. Several firms tell us credit insurance is increasingly seen as a tool to bring greater predictability at a time when customer payment behaviour has become less reliable and more volatile.

For a full overview of the 2026 survey results for Belgium and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.