Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

The clear finding from our survey is that Spanish companies remain highly aware of customer payment risk but continue to trade with enough flexibility to keep business flowing. The pressures they face mirror those across Western Europe, shaped by tight liquidity and unsettled economic conditions. Spain’s response blends caution, close monitoring, and selective use of credit in a way that suggests not only resilience but a strong understanding of how to contain risk without stalling B2B trade.

In an economy dominated by small firms, often with less credit management processes, Spanish firms extend credit mainly where trust exists and risk feels manageable. As a consequence, 47% of B2B sales are made on credit, five percentage points below the Western European benchmark. Despite the overall mood of caution, many Spanish firms increased their trade credit offering in recent months in response to customer demands. This reflected selective adjustments to competitive pressure rather than a broad shift in risk appetite.

.2026-06-03-08-46-46.png)

Payment terms remain short, suggesting that businesses prioritise a quick invoice-to-cash turnaround. Most companies, broadly in line with Western Europe, offer payment terms of 30 days or less and collect payments within this window, as reflected in the average Days Sales Outstanding (DSO). Some easing occurred during the recent months, driven mainly by SMEs. This led to greater use of terms of up to two months from invoicing than in many neighbouring markets.

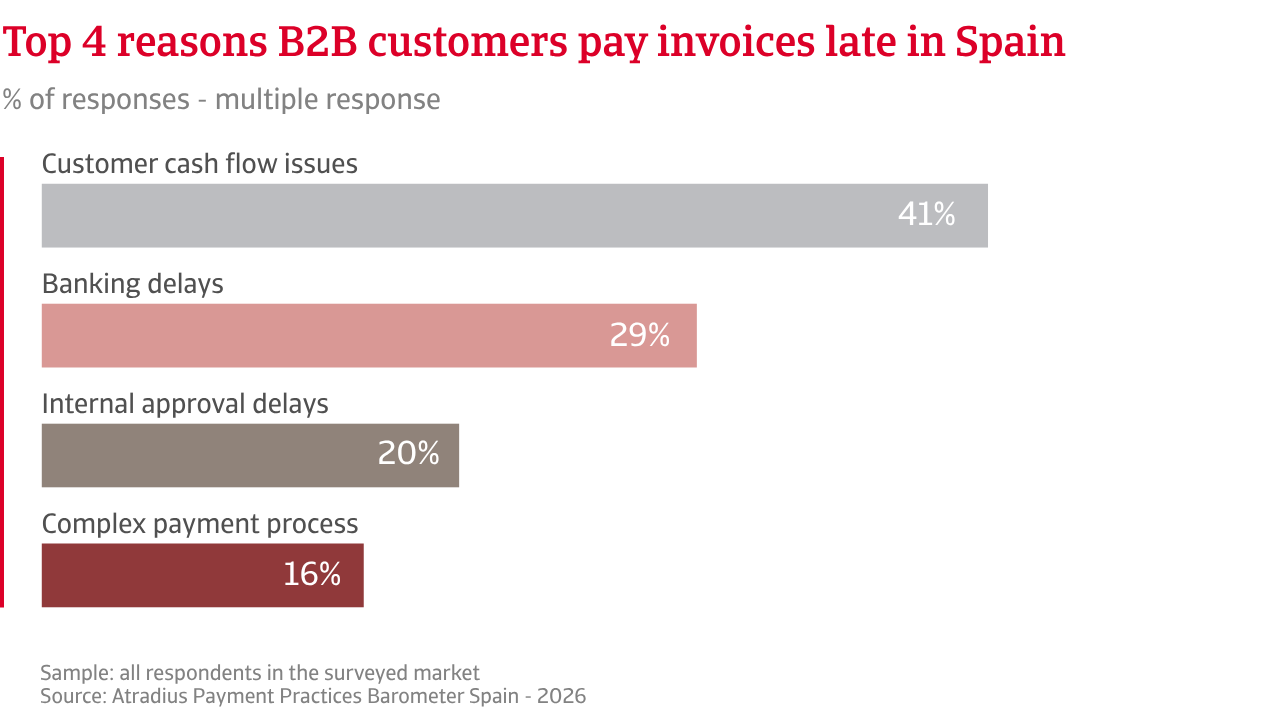

Spanish businesses report late payments less often than their Western European peers. 61% of firms are affected, compared with 77% across the region. Fewer invoices fall overdue, well below the regional benchmark of one in four paid late. However, when payments slip, settlement timelines broadly match the regional average. This suggests that B2B payment risk in Spain appears contained, but resilience is thin once cash is delayed.

Liquidity pressures drive most delays, as tighter credit conditions prompt customers to slow invoice payment. Bad debt losses remain at or below 2% of B2B turnover. A small group, mainly SMEs in construction and trade report higher shares, suggesting pockets of concentrated risk that need close monitoring. The overall profile is broadly close to Western Europe.

Risk mitigation approaches also differ from regional peers. Across the region, firms rely more on automated reminders, digital payments and stricter payment policies, reflecting a stronger focus on prevention. In Spain, the emphasis is more on protection. A higher share of businesses report setting aside provisions for bad debt and using credit insurance to cushion the impact of payment delays. The balance reflects how much risk businesses are willing, and able, to carry on their balance sheets.

In an economy dominated by small firms, often with less credit management processes, Spanish firms extend credit mainly where trust exists and risk feels manageable.

Like their Western European peers, Spanish companies have spent recent years operating in an unstable economic environment. That experience shapes expectations for the months ahead, with most remaining cautious, with uncertainty still high. Across sectors, businesses do not expect B2B payment behaviour to improve in the short term, and expectations are more restrained than in much of Western Europe. B2B late payments are widely seen as part of the operating landscape rather than something likely to ease soon.

Views on insolvencies reinforce this cautious outlook. Most firms expect insolvency levels to remain high in the short term. Some foresee further increases, while many remain unsure about how conditions will evolve. High insolvency levels reflect the impact of rising costs, tighter access to finance, and the gradual withdrawal of support measures. The 2022 legal reform, which simplified insolvency procedures, has also made it easier for distressed firms to file.

Expectations on profitability remain modest. While some businesses anticipate slight improvements, few believe those gains will last. Any improvement depends on costs staying under control and customers paying on time. However, expectations differ by company size. Larger firms benefit from steadier order flows and greater financial flexibility. Smaller businesses rely more heavily on domestic demand and feel payment delays more acutely.

Spanish businesses expect future B2B payment trends to be shaped primarily by broader economic and geopolitical conditions rather than isolated shocks. Spain’s economic outlook remains relatively resilient, supported by private consumption and services activity, but growth is slowing and borrowing costs remain high. These factors are expected to weigh on short-term business liquidity, particularly among SMEs.

Looking ahead, Spanish firms are less influenced by inflation concerns than elsewhere in Western Europe. Attention is focused instead on macroeconomic headwinds, including a significant slowdown and tighter financing conditions. Sector-specific downturns also play a more prominent role. Even as tighter financing and uneven sector performance continue to pose challenges, businesses remain confident about navigating the months ahead. The prevailing mood is not confidence, but caution and readiness to manage continued economic volatility and trade uncertainty.

For a full overview of the 2026 survey results for Spain and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.