Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

B2B payment behaviour across Western Europe is shifting. As access to finance tightens, customers rely more on trade credit in business-to-business (B2B) transactions. This keeps trade moving, but it also pushes more risk onto suppliers. As customer payment risk spreads across the corporate landscape, companies tighten credit control, track cash more closely, and take a more selective approach to risk as core to resilience.

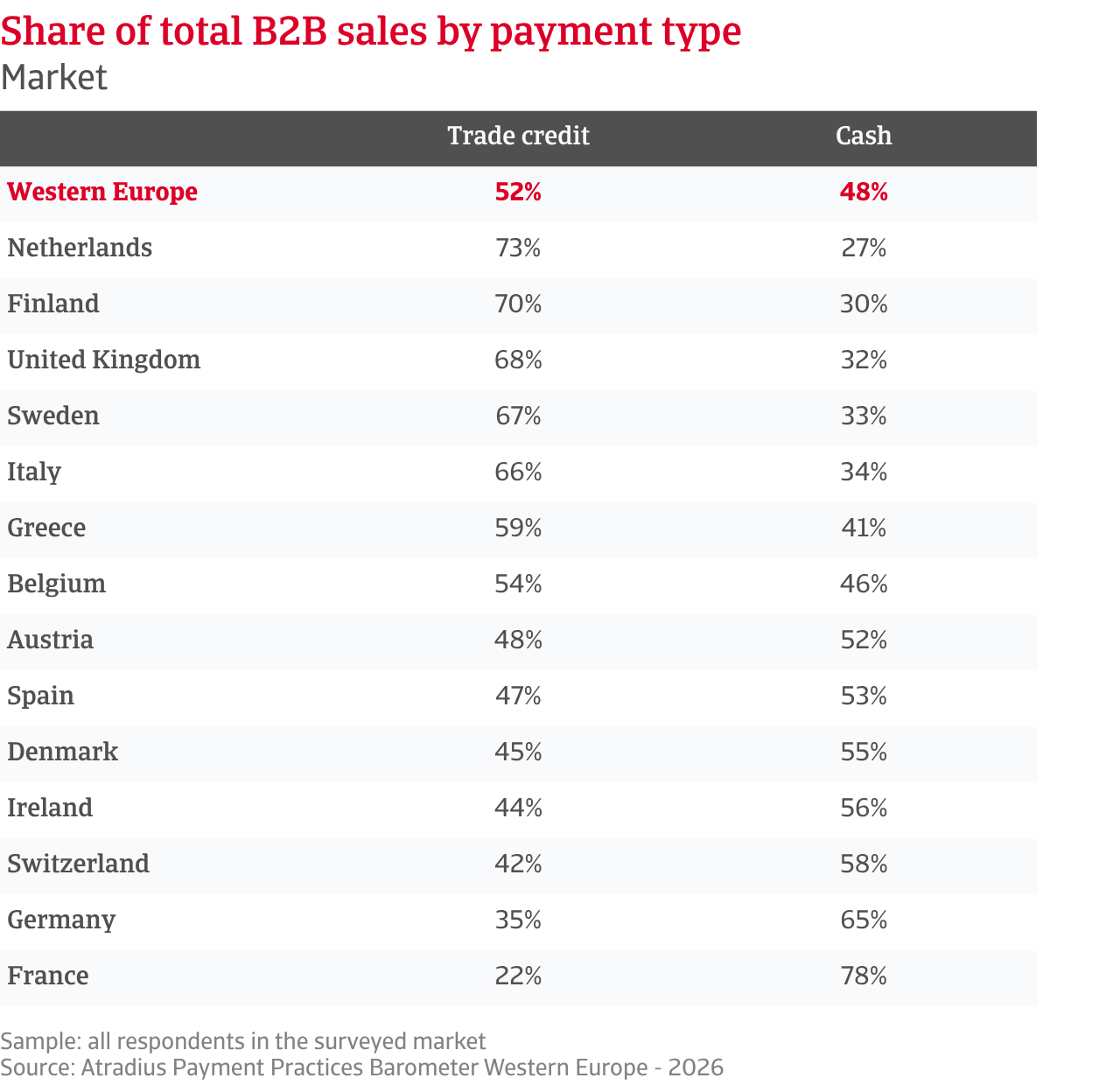

Just over half of B2B sales across Western Europe, around 52%, now take place on credit. This average hides wide differences between markets. The Netherlands stands out clearly, with nearly three quarters of B2B sales settled on deferred terms, the highest share in Western Europe. France sits at the other end of the scale, where only 22% of B2B sales are made on credit. Most markets across the region continues to increase their use of supplier credit, with Sweden showing one of the strongest shifts. Switzerland takes a more cautious approach, reflecting stronger concern around customer payment risk.

.2026-05-12-07-17-45.png)

Payment terms across Western Europe remain relatively tight. Most businesses report setting payment terms within a 30-day credit window, which highlights a clear reluctance to ease terms despite rising pressure from customers. Fewer companies across the markets surveyed in Western Europe extend payment terms to up to two months from invoicing and longer credit periods remain uncommon. Italy is the clear exception, as businesses offer significantly longer terms than the regional average. Regionally, most markets remain closely aligned with the Western European benchmark, with little evidence of a broad shift towards structurally longer payment cycles.

As liquidity pressure feeds into day-to-day operations, payment behaviour among Western European business customers has weakened in recent months. Nearly four in five companies across the region report B2B customers pay invoices late. Companies in Switzerland express the most negative sentiment, pointing to strain even in markets seen as traditionally resilient. Ireland stands out as the main exception, with more positive payment experiences, while most other markets sit close to the regional benchmark.

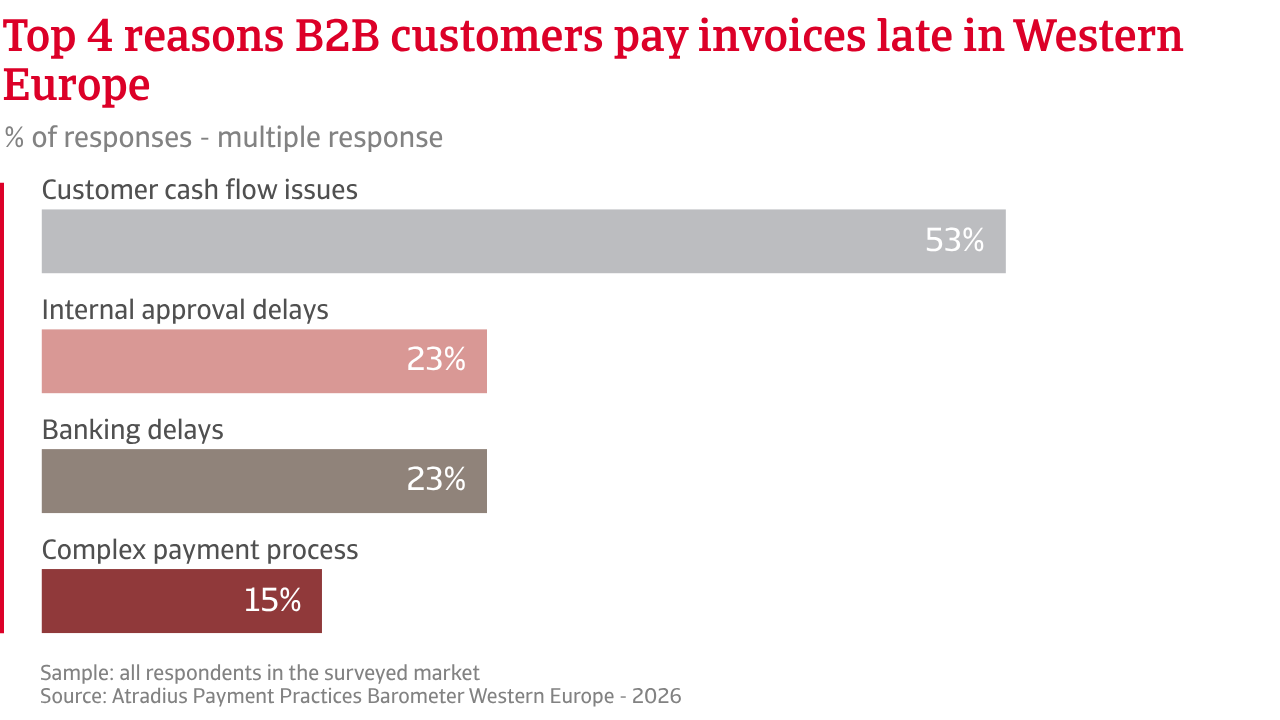

More than half of the businesses surveyed across Western Europe report that liquidity pressure is the main reason behind late payments from business customers. Italian companies feel this pressure most strongly, while Irish firms appear least affected. Administrative bottlenecks, banking delays and technical issues related to e-invoicing or digital payment platforms add to settlement delays, even where cash is available.

.2026-05-11-07-58-43.png)

The share of working capital tied up in overdue B2B invoices varies across Western European markets. Regionally, about one quarter of invoices are paid after the due date. Greece records the highest share, locking up significant working capital, while the Netherlands stands out for its strong payment culture with the lowest incidence of past due payments in the region. Most other markets cluster close to the regional average. Once invoices fall overdue, settlement times appear broadly similar, averaging around one month beyond the due date. Italy records the longest delays, while the Netherlands ranks among the fastest. Overall, pressure on working capital is driven mainly by how often payments are delayed than by how quickly they are recovered.

Survey evidence shows that payment cycles, measured through Days Sales Outstanding (DSO), have continued to edge higher across Western Europe in recent months. Businesses report collecting cash slightly later than agreed, which pushes DSO slightly above agreed payment terms, increasing pressure on liquidity. While most Western European markets cluster around the regional average of just over one month, the remainder sit at either end of the range, reflecting longer or shorter payment cycles. Italy stands out as the clearest example, with payment cycles stretching more than in any other major market.

As DSO rises, the risk of bad debts also increases. Across the region, credit losses now average 1.6% of B2B invoiced turnover. Nearly one in four report losses of up to 5%, a level that steadily erodes working capital and profitability. Germany and Sweden are among the most exposed within this range. Losses above this threshold remain less common, though most often reported in Belgium.

Weaker B2B payment behaviour is now placing significant strain on working capital across Western Europe. Many companies, particularly in Greece, report less cash available for daily operations, reduced planning visibility and rising use of external finance, often at higher cost. Elsewhere, limits on investment are becoming more visible, particularly in Switzerland. Payment pressure also increasingly passes down supply chains, most clearly in Belgium.

In response, businesses across Western Europe report managing risk more carefully, without slowing trade. Most start with internal measures, such as active credit control, payment monitoring, and selective limits by customers. Tools like credit insurance, guarantees, or advance payments are typically used more selectively, often reserved for larger transactions or higher-risk customers. Overall, Western European companies are trying to stay flexible and keep trade relationships intact, while tightening control where pressure is clearly rising.

Across Western Europe, confidence remains low. Many businesses feel uncertain about what lies ahead and say they operate under ongoing pressure, trying to stay balanced in a challenging economic and trading environment.

In this climate, more than half of the firms surveyed, regardless of market or sector, do not anticipate any meaningful short-term changes in the payment behaviour of B2B customers. Expectations appear most settled among Dutch businesses. Elsewhere across the region, views vary notably from one market to another. In France, for instance, businesses are more likely to fear a worsening of B2B payment behaviour, as customers remain under pressure from tight financing and high operating costs. Geopolitical disruption continues to add strain, while volatile energy prices and fragile supply chains make planning more difficult. As a result, many companies say they no longer rely on a single outlook and instead prepare for several possible scenarios.

What stands out across the region is how many companies say they cannot see very far ahead. High uncertainty feeds directly into everyday B2B trade credit decisions. Extending credit feels riskier, and cash flow is monitored more closely. Seen up close, many businesses say they are operating with little buffer. Costs continue to rise; margins no longer offer much protection and sooner or later prices have to move. That leaves companies exposed to risk, knowing that any pushback or late payment can quickly affect cash flow.

A similar sense of unease comes through when businesses talk about insolvencies. Most companies across the region, particularly in the Netherlands, expect insolvency levels to remain where they are now, already higher than many would like. Among those expecting change, pessimism outweighs optimism. More businesses anticipate a further rise in insolvencies than believe conditions will stabilise or improve, a view felt most strongly in Finland. Others simply say they do not know what lies ahead, which may be the most telling response. Profitability expectations complete the picture. Most companies across Western Europe do not expect any meaningful change in the short term. Where views are not openly pessimistic, as among Greek businesses, uncertainty prevails, a mood particularly widespread in the UK.

All of this unfolds against an economic backdrop that feels uneven and highly fragmented. While services activity keeps the region moving, manufacturing and trade remain under pressure. Fears of a sharper economic contraction in the months ahead are felt most strongly among Italian businesses, while geopolitical instability cuts across markets almost uniformly, affecting businesses regardless of size or sector.

Overall, survey feedback from across Western Europe highlights that unpredictable shifts in B2B payment behaviour have become one of the clearest signs of underlying strain. Many businesses describe uncertainty as a constant feature of daily operations. Those that accept this reality, and manage payment risk with that mindset, are better placed to hold their ground in the current unsettled environment.

For a full overview of the 2026 survey results for Western Europe, please download the regional report and the statistical appendix from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.