Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

The Payment Practices Barometer for the Nordic region features Denmark, Finland, and Sweden. It explores how businesses in these markets manage B2B trade credit and payment risk, and cope with increased pressure on corporate liquidity.

Selling on credit remains a standard feature of business-to-business (B2B) trade in Denmark. An average of 44% of B2B sales are made on credit, well below Western European and other Nordic markets. Recent growth in credit use reflects competitive pressure, as offering trade credit helps protect sales and long-standing customer relationships. Most Danish firms continue to work with 30-day payment terms. Longer terms appear more often than elsewhere in Europe and the Nordics, reflecting flexibility supported by reliable payment behaviour. Overall, payment performance remains stronger than in Western Europe and broadly in line with Sweden, while outperforming Finland.

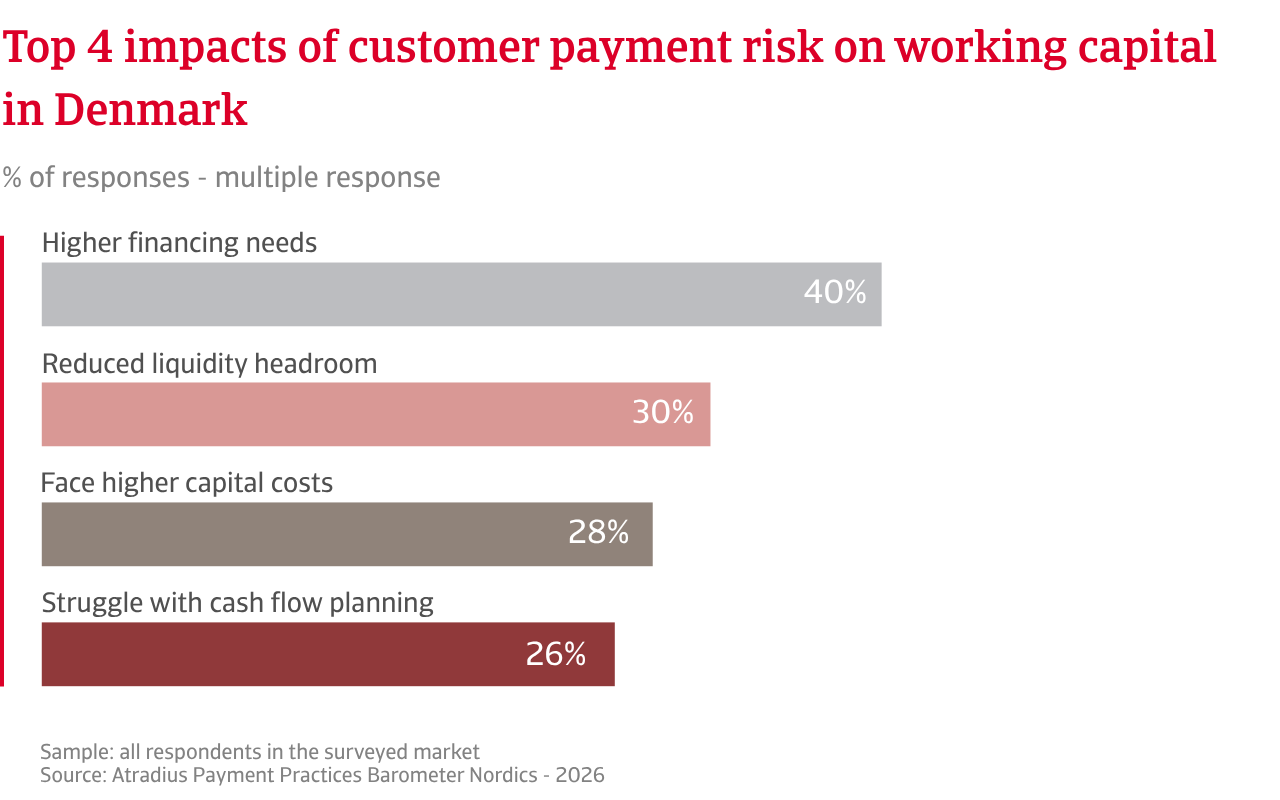

Late payments affect three quarters of firms. Delays mostly arise from banking processes or internal procedures, rather than customer liquidity distress. Most overdue invoices are settled within a month past due, and DSO remains close to agreed terms. Credit losses are limited, usually below 1%. This shapes how payment risk feeds into working capital. In Denmark, customer payment risk mainly increases reliance on external funding and raises financing costs, while cash flow and investment stay protected. Across Western Europe and the Nordics, payment risk more often tightens liquidity and affects operations. Danish firms respond through active credit management, using insurance to prevent losses rather than transfer risk, as more common elsewhere.

Broadly in line with other Nordic markets, most Danish firms do not expect any meaningful short-term change in B2B customer payment behaviour. Among those expecting a shift, views are almost evenly split, reflecting greater uncertainty in a more challenging economic environment. Most Danish businesses expect insolvency levels to remain steady in the short term, broadly in line with Western Europe and Sweden, while confidence is weaker in Finland. Compared with Western Europe and Finland, fewer Danish companies expect insolvencies to trend upward, placing Denmark closer to Sweden in terms of expectations.

Most Danish firms also expect profit margins to hold steady, with far lower downside risk than in Western Europe. This reinforces Denmark’s resilient operating environment, as peers across the Nordics are more likely to anticipate margin pressure in the short term. Compared with Western Europe, Danish firms view B2B payment risk as process led, with liquidity pressure largely stemming from inflation driven increases in business costs, rather than economic weakness. Across the Nordic region, Swedish businesses share a similar view, while in Finland payment risk expectations are more strongly associated with weaker economic conditions and sector specific stress.

Finland’s heavy use of trade credit shapes how economic pressure spreads across the economy. Around two thirds of business-to-business (B2B) sales now take place on credit, the highest share among the Nordic markets and above Western Europe. Trade credit use continues to grow, outpacing Western Europe but trailing Sweden. This means Finnish suppliers often finance business customers. In line with Nordic and Western European practice, most Finnish companies set payment terms within a 30-day credit window. Longer terms remain far less common in Finland, reflecting a preference for liquidity protection combined with selective customer relationships.

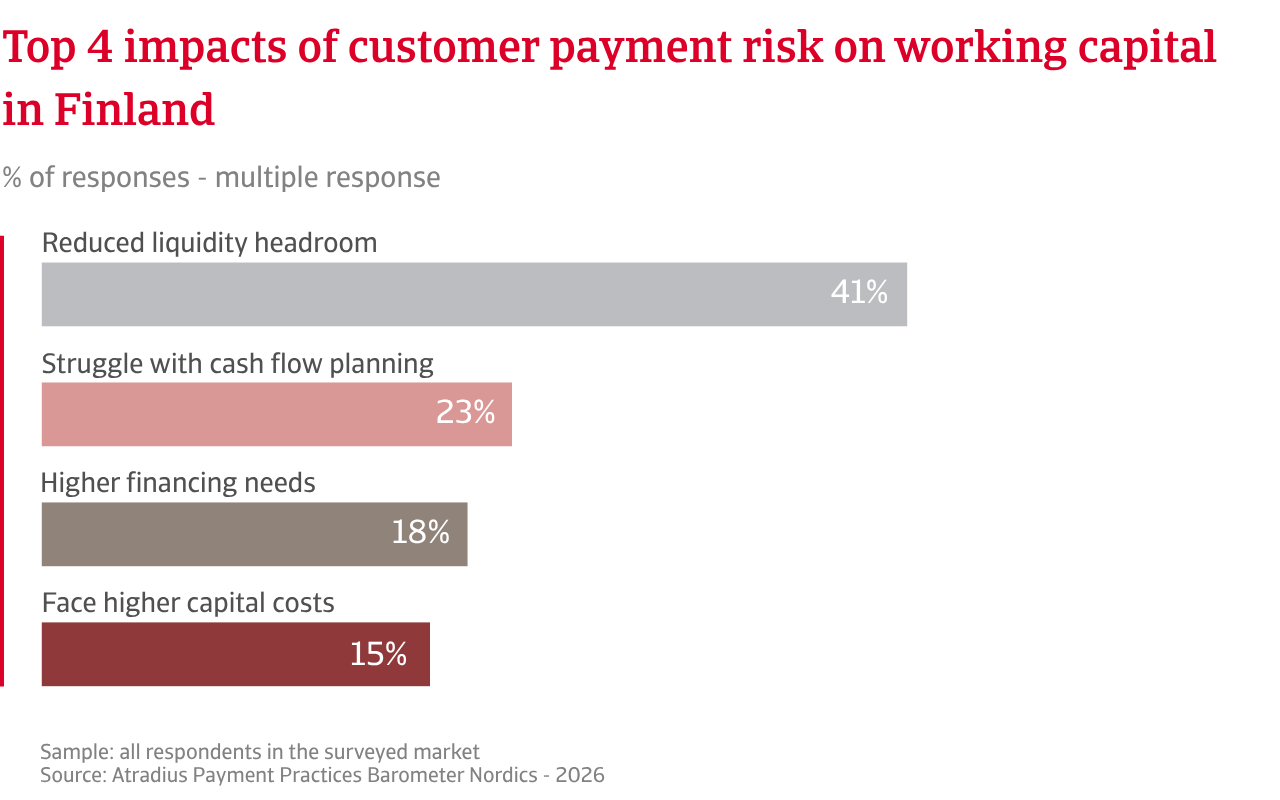

Just over three quarters of firms report B2B late payments which affect one fifth of invoices, the lowest share across the Nordics and Western Europe. Delays mainly reflect customer liquidity stress. Most overdue invoices are settled within one month past due, while Days Sales Outstanding (DSO) stays broadly close to agreed terms. Credit losses remain limited, often below 1% of credit sales, mainly driven by customer insolvencies. Working capital pressure shows up mostly as reduced cash for daily operations. To mitigate customer payment risk, Finnish firms rely mainly on active credit management and insurance rather than setting aside reserves, while Western European and Nordic peers spread risk across wider or more mixed strategies.

Most Finnish companies surveyed do not expect any significant short‑term change in payment behaviour of B2B customers, a viewpoint reflecting uncertainty rather than confidence. This is highly likely driven by concerns over slower economic growth and sector‑specific pressures. Insolvency expectations underline this unease. Nearly half of Finnish companies expect a further rise in insolvencies in the short term, a far higher share of respondents than across the Nordics and Western Europe. Among the remaining survey respondents, most expect insolvency levels to remain largely unchanged, while only a small minority express outright uncertainty.

Profit expectations tell a similar story. A clear majority of companies across Finland expect profit margins to remain unaltered in the short term, a larger share than in the Nordics and Western Europe. Among firms anticipating shifts, negative expectations outweigh positive ones by a wide margin, in contrast to the more balanced outlook seen elsewhere. When asked which factors could affect B2B payment behaviour in the short term, Finnish companies stand out for their strong focus on domestic economic weakness. Sector‑specific stress features more prominently in Finland than among Nordic peers, which report a broader mix of risks. In contrast, businesses in Western Europe point to several pressure points at once and show greater sensitivity to external factors.

Swedish firms use trade credit extensively in both domestic and export business-to-business (B2B) transactions. Around two thirds of B2B sales are made on credit, representing an increase in recent months, outperforming Western Europe and other Nordics markets to sustain demand in a challenging economic climate. Most Swedish companies set payment terms within a 30-day window, broadly aligned with practice across the Nordics and Western Europe. Longer terms are also common, more than elsewhere in both regions. However, these have not translated into faster payments in most cases, as Swedish firms report increased delayed payments recently. Customer liquidity stress impacts Nordic suppliers, while the Western European payment landscape appears relatively more stable.

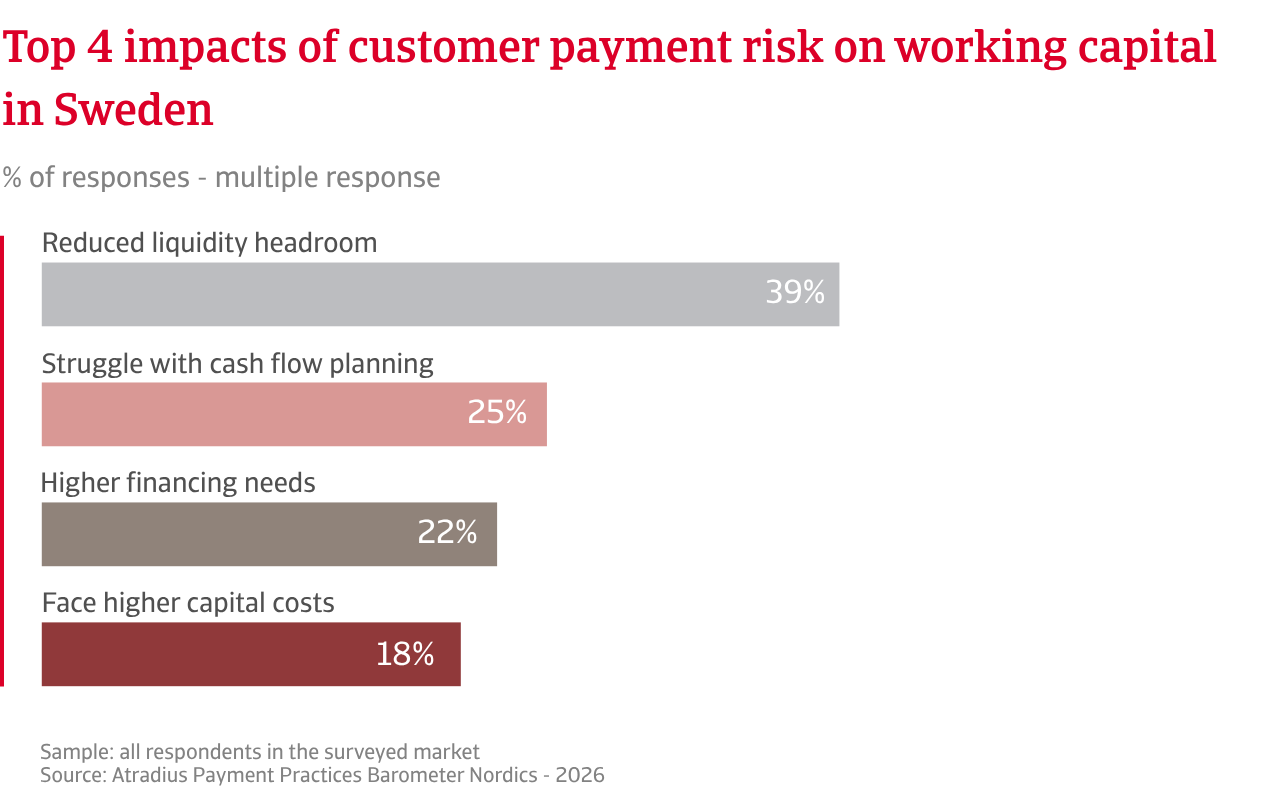

In Sweden, just over one quarter of invoices are past due, affecting more firms on the market than elsewhere in both regions. Long term payment delays, that are chiefly due to customers’ cash flow issues, ended up in credit losses affecting an average of up to 2% of invoices. Bad debts write-offs are mainly driven by disputes and customer failure. The working capital impact creates operational and funding pressure. To mitigate customer payment risk, Swedish firms focus on credit control and monitoring, rather than set buffers that lock up capital. Credit insurance use sits between Finland and Denmark, broadly mirroring Western European patterns.

Although most businesses in Sweden do not expect a significant short-term shift in B2B payment behaviour, broadly in line with peers across Western Europe and the Nordic region, the overall mood remains more confident. This comes from firm’s belief in the ability to manage customer payments through strong internal control, even as Sweden’s export-oriented economy leaves cash flow exposed to weaker payment behaviour among key trading partners. Most Swedish firms also expect insolvency levels to remain broadly stable in the short term, mirroring expectations in Western Europe and Denmark. Finland stands out with a more pessimistic outlook. At the same time, Swedish businesses express strong uncertainty about this topic.

Profit margin expectations also point to stability across Western Europe. In Sweden, some pressure is anticipated, but more firms express cautious optimism. Denmark largely mirrors the Western European picture, while Finland again shows a more volatile outlook, underlining greater uncertainty around short-term profitability. In response, Swedish businesses focus on risks they feel able to control, including selective adjustments in payment terms and closer monitoring of customer credit, rather than broad based tightening, while Western European peers appear more concerned about the wider economic environment and take a more cautious, across the board approach.

For a full overview of the 2026 survey results for Nordics and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.