Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

Although due to come into force at the beginning of October, the tariffs (which range from zero to 100%, with the 0% rate designed to bolster the made in America brand) are currently paused. The pause is likely to represent the calm found in eye of the storm. Pharmas throughout the world are now scrambling to calculate the impact of this latest announcement on their profits, trade routes and even the locations of their manufacturing sites before President Trump takes his finger off the pause button.

A good place to start assessing these latest tariff announcements is to understand the importance of the US within the global pharmaceutical market. North America is by far the largest market for pharmaceuticals, accounting for more than half of all of the world’s retail, hospital and prescription sales. The US is also an important node on the complex worldwide network of pharmaceuticals supply chains. Active pharmaceutical ingredient (API) manufacturing, packaging and clinical development often take place across several countries.

We can safely say, therefore, that the imposition of US pharma tariffs, has the potential for far reaching and even critical impacts on the industry in every corner of the world. “To put it simply,” said Judy Ji, Atradius Senior Underwriter in Shanghai, China, “tariffs affect logistics, trade flows, production costs and business margins. They can lead to potential shortages and delays.”

Up until the end of September, pharmaceutical goods have been exempted from the so-called reciprocal tariffs announced by President Trump back in April. This is mainly because earlier this year, the US government opened a national security probe, (Section 232) examining the possibility of tariffs on pharma goods and the tariff pause button was hit pending the outcome of the probe.

However, regardless of the Section 232 investigation (the outcomes of which still loom), on September 26 the Trump administration has now announced a sweeping new tariff policy targeting pharmaceutical imports into the US. The announcement stated that from October 1, all branded or patented drugs imported into the US will face 100% tariffs, unless the manufacturer has US-based manufacturing facilities (or has US facilities ‘under construction’.) This was then temporarily paused and it is currently unclear when the 100% tariff threat will be enacted.

In addition to this US-based manufacturing focus, the recent announcements require pharma firms to practise what President Trump calls “most favoured nation (MFN) pricing”. In effect, this requires pharmas to align their US prices to those charged in other developed nations.

The September 26 announcement has already seen some large pharmaceutical producers, most notably Pfizer, announce a reduction in prescription drug prices for US consumers and a commitment to invest additional financial resources in US manufacturing.

A large proportion of the profits of many global pharmaceutical companies are earned in the United States, where, unlike in many European countries, drug prices are hardly regulated by the government. The introduction of the 15% tariffs, or especially an escalation to the 100% tariffs makes exporting into this lucrative market more costly and more complicated.

“The 15% tariff costs for EU business exporting pharmaceuticals to the US could reach EUR 18 billion.”

Rubén del Río Hernández, Team Leader Large Buyer Unit at Atradius CyC, Madrid, Spain explained: “The fact is, EU producers of patented drugs are still unsure as to whether the 100% tariff costs would apply to them, or whether this would remain at the 15% rate previously agreed between the US and the EU. Estimates suggest the 15% tariff costs for European businesses on pharmaceutical exports to the US would amount to EUR 18 billion.” That represents a pretty sizeable dent in the industry’s profit margins.

Rubén added: “The Trump administration, in an attempt to boost its pharmaceutical industry at the expense of the European one, could also establish selective price limits, undermining the profits of European pharmaceutical companies or those that do not manufacture drugs on US soil.”

The bulk of Chinese and Indian pharma exports to the US is mainly generics rather than branded or patented goods. For example, in China patented drugs amount to only 0.2% of the country’s total pharma exports to the US. This means that pharma exporters from both countries seem to be safe for the time being given that President Trump’s recent tariff threats currently exempt generics.

However, uncertainty remains. After the recent announcement, the global industry is questioning whether complex generics and biosimilars will face future tariffs. The distinction between branded and generic drugs is not entirely clear. There are a lot of branded drugs that are actually generics or off-patent drugs that are traded under a brand name, for example. It's unclear whether these will be categorised as branded or generic under the most recent tariff rules, and whether or not they would attract the 100% tariff levy.

Judy said: “Despite the temporary pause on enacting the 100% tariffs, Chinese and Indian pharma exporters to the US would be prudent to remain prepared for future policy shifts and to build risk-mitigation strategies.”

In addition to squeezing the profit margins of exporting producers, US tariffs would impact supply chains. Active ingredient manufacturing, packaging and clinical development take place in different countries. Inevitably, tariffs affect logistics and margin flows.

Brady McKinney, Atradius Underwriter in Baltimore, USA said: “Heightened supply chain protectionism, particularly between the US and Mainland China, would drive pharmaceutical companies to establish separate supply chains to mitigate risk. This would result in less efficiency in global pharma manufacturing networks.”

He added: “Firms are already shifting from cost-centric to risk-centric models, prioritising resilience over margin. Nearshoring to Latin America, Eastern Europe, and Southeast Asia is gaining traction as a lower-risk alternative to reshoring.”

Both the size of tariffs and the erratic nature of the policy announcements and implementation are destabilising for the industry. Many businesses are adopting a ‘wait and see’ approach, pausing investment and expensive R&D until they have a clearer understanding of what the tariff landscape will look like.

The tariff threats are also driving a trend towards nearshoring and reshoring as pharmaceutical companies seek ways to mitigate risk. Although this could erode efficiency in manufacturing networks, many pharmas are rebuilding their operating models to prioritise resilience over margin. For many, this included plans to expand their operations into the US, even before Trump’s September 2025 policy announcements offering tariff exemptions for pharmaceuticals companies investing in the US.

Brady noted: “As of July 2025, the largest multinational drugmakers have pledged over USD 400 billion to expand their R&D and manufacturing capacity in the US. Next to tariffs, it’s expected the Trump administration will leverage stricter oversight for foreign manufacturing sites and decrease regulatory hurdles for domestic facility construction in order to incentivise reshoring into the US.”

He added: “What is currently unclear, however, is what President Trump means when he said that firms that have a manufacturing site in the US or are in the process of constructing one would be exempt from the tariffs. Although he has acknowledged that this applies to projects that have broken ground or started construction, he has not confirmed whether the tariff exemptions apply to all of a company's products, or products that are at least partly made in the US, or just those products that are wholly manufactured in US-based facilities.”

However, the US tariffs are not just incentivising pharmaceutical businesses to invest in the US. Pharma firms are also increasingly turning towards China and entering licensing agreements with China-based companies. This reflects a confidence in the market’s extensive manufacturing infrastructure and advancing R&D capabilities. Progressive drug approval processes will continue to elevate the country's status as a global pharmaceutical powerhouse.

“Multinational partnerships and licensing agreements in China reflect a confidence in the country’s biopharmaceutical ecosystem.”

Judy Ji said: “Clinical research in China's pharmaceutical sector will likely see increased prominence, supported by government incentive policies and initiatives. This shift is evidenced by the growing trend of multinational drugmakers' licensing agreements with China-based firms, a testament to the market's growing R&D capabilities and the value of its biopharmaceutical assets. These partnerships reflect confidence in the country's biopharmaceutical ecosystem.”

European businesses, in particular, face competitive disadvantages as more pharma businesses invest in the US and China, at the expense of investments in Europe over the coming years. Despite well-established manufacturing facilities, secure supply chains and high production standards, the EU is facing gradually decreasing competitiveness in innovation. This is due to slower clinical trial setup times, weakening its ability to develop and produce new drugs early, in addition to less favourable regulatory and funding environments, and smaller patient pools compared to the US and China.

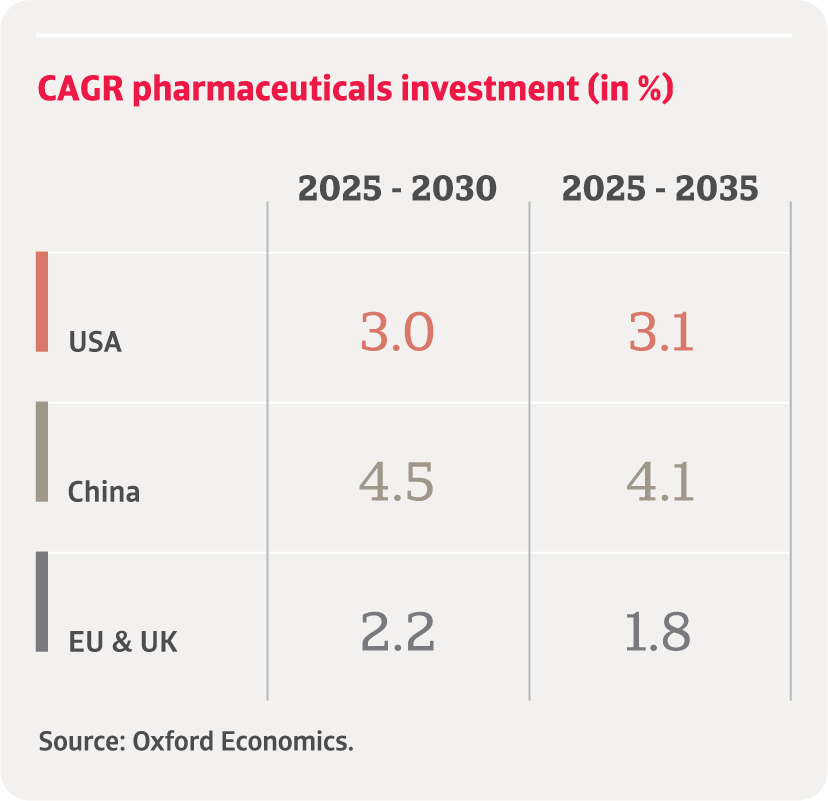

The squeeze on the European pharmaceutical sector can be seen in the predicted compound annual growth rates (CAGR) for the world’s major manufacturing regions. 2025-2030 forecasts indicate CAGR for China pharma investments at 4.5%, the US at 3.0% and the EU and UK at 2.2%.

The pinched margins and supply chain challenges experienced as a result of the tariff threats and related insecurity are now evolving into heightened credit risk across the industry.

From his base in Madrid, Rubén del Río Hernández said: “Smaller EU manufacturers, or those reliant on single-site production in Europe, could experience sustained margin pressure as tariffs erode cost advantages and complicate trade logistics with the US. Moreover, moving manufacturing to the US will require substantial capital investment and operational restructuring, also posing challenges for smaller companies with limited resources.”

He added: “Small manufacturers will eventually face price pressures (in the form of higher raw material costs) due to the changing environment, where larger groups will open new facilities in other countries (especially China) that could modify supply lines and push input prices upward. Producers of generic drugs or those whose revenues depend on a limited number of products will suffer the consequences of the current scenario more severely—especially small and medium-sized pharmaceutical groups that manufacture in Europe and sell their products abroad (even more so if the United States is among those markets).”

Judy Ji, our sector specialist in China, acknowledges the challenges facing smaller European producers but notes that China’s size does not offer immunity to the credit risks that the US tariffs present. She said: “Although the traditional portion of the pharmaceutical industry, including drugs producers, would be less affected by the tariffs than their EU counterparts, especially as the majority of exports to the US feature generics and non-branded medicines, the same cannot be said for medical devices.”

She explained: “The Chinese medical device sector is experiencing heightened credit risk due to the tariffs. The US remains the largest export market, accounting for 24% of China’s medical device exports in 2024. Tariffs have raised the cost of Chinese products, eroding their price competitiveness—particularly for low-margin consumables such as gloves and syringes. As a result, many small and mid-sized manufacturers face declining orders and potential closures.”

To mitigate the impact, Chinese companies are accelerating overseas production setups. Over 300 Chinese medical device companies have shifted production to countries like Vietnam. However, challenges such as rules of origin requirements continue to pose obstacles.

In the short term, higher burdens on profits and capital costs would make medicines in the US more expensive, especially in light of the tariffs imposed by the most recent White House announcements and any additional levies applied following the Section 232 investigation. Brady McKinney in Baltimore noted: “US producers that are reliant on imports would be facing sharp cost hikes, threatening their profitability. If increased costs are filtered through the system, healthcare providers, insurance companies, and even pharmacies would be negatively impacted, meaning credit risk may not be confined to pharmaceuticals manufacturers, but could have an impact on the industry in its widest form.”

“Credit risk may not be confined to pharmaceuticals manufacturers but could impact the wider industry.”

Brady added: There is also an increased credit risk for companies involved in R&D such as Contract Research Organisations (CROs), lab equipment suppliers, other scientific instruments, Contract Development and Manufacturing Organisations (CDMOs).”

He said: “Some companies are also reassessing their tax structures in light of the tariffs in a bid to lower credit risk. For example, some pharmaceutical companies are considering returning their patents and other intellectual property, along with the associated revenues (from charging sister companies licensing fees) to the US. Even if doing so increases their tax burdens, higher corporate taxes might cost less than tariffs.”

He concluded: “Although there could be some long-term benefits to homeshoring pharma production, including securing supply, high US production costs could still make it more cost-effective for pharmaceuticals to be manufactured elsewhere.”

Download the full report in the related documents section below for a detailed analysis of the challenges, performance, and credit risks facing the pharmaceutical industry throughout the world.

To explore how these insights can strengthen your own credit risk strategy, get in touch with us to see how we can help you stay ahead.