Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

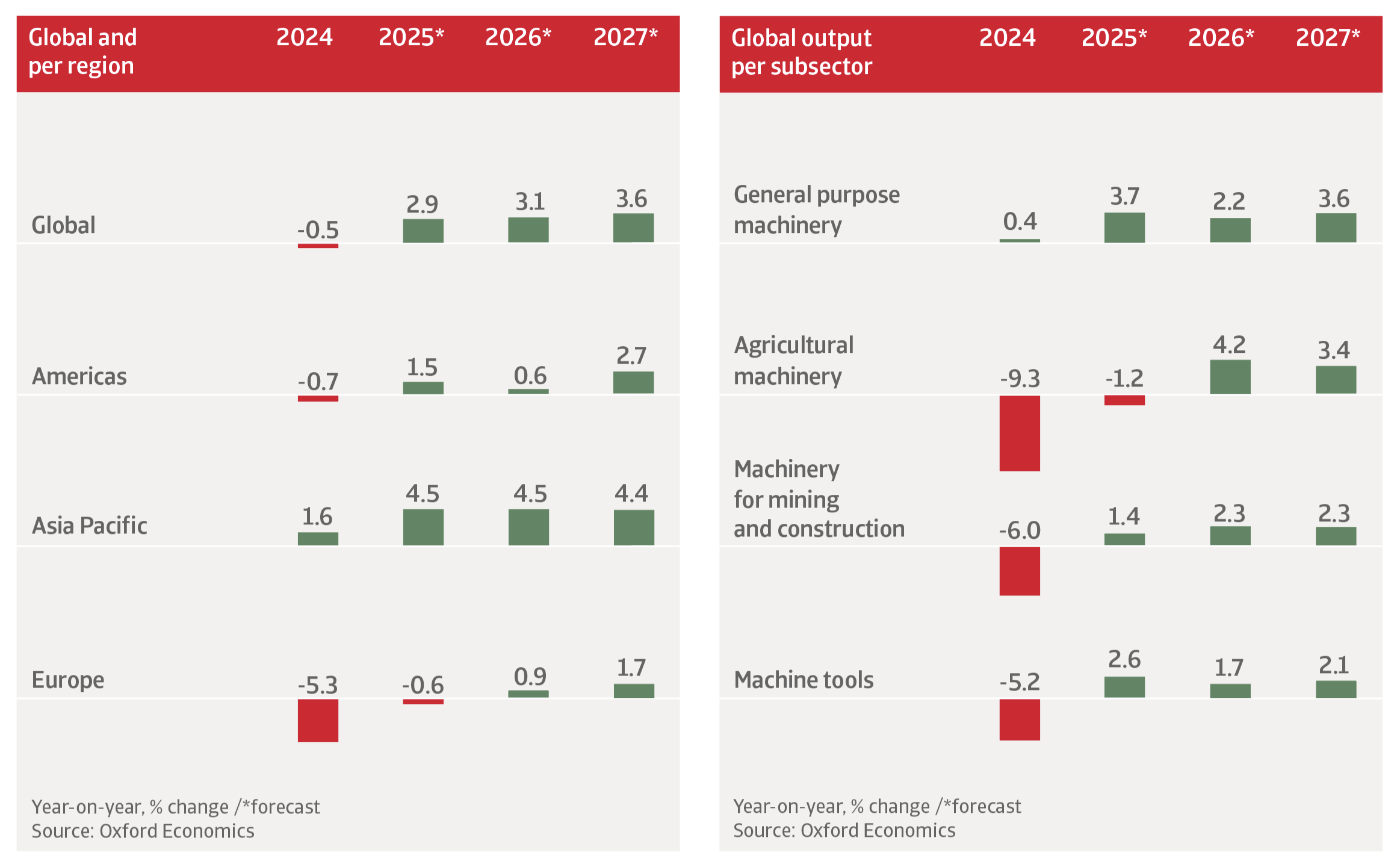

We expect global mechanical engineering output to increase by 3.1% in 2026. Growth remains below potential, as the sector continues to face a complex mix of ongoing trade uncertainty, geopolitical risks and elevated capital expenditure costs.

Machinery is highly reliant on cross-border supply chains, and therefore very sensitive to changes in global trade policies. Companies are facing renewed uncertainty surrounding tariff regimes and legal risks.

In this business environment many companies in the manufacturing sector remain reluctant to invest in capital goods. In addition, the monetary policy easing cycle has slowed in most countries for the time being.

In 2027 we expect global mechanical engineering output growth to accelerate to 3.6%, as additional monetary easing expected in H2 of 2026 begins to feed through and defence spending increases, particularly in Europe.

In the mid- and long-term, the shift towards electric vehicles will lead to changes in machinery supply to the automotive sector, with more emphasis on batteries and related electrical equipment. Demand for machinery to manufacture conventional powertrains will weaken.

We expect US mechanical engineering production to grow by 1.3% in 2026 and by 2.4% next year. After increasing by 8% in 2025, machinery and equipment investment in the US should expand again this year. A main driver is ongoing robust AI-related capital expenditure, particularly in hardware and data-centre construction.

The so-called One Big Beautiful Bill Act (OBBBA) includes some generous provisions for deducting the cost of machinery and equipment purchases. The extension of tax cuts and the increase in government spending (defence and non-defence) supports demand for US machinery across all subsectors in the forecast period.

However, the current US tariff policy risks preventing additional growth of machinery production and sales due to higher input costs. Producer price inflation for machinery and equipment has sharply increased since mid-2025. Steel and aluminium are still tariffed at 50%, which will continue to put upward pressure on input costs and weigh on competitiveness.

In the mid- to long-term, demand for automation, digitalisation, and sustainable production solutions in manufacturing should support machinery demand in the US. New technologies integrated in the manufacturing process and generative AI will increase productivity in the mechanical engineering industry.

We expect Canadian mechanical engineering production to contract by 7.9% in 2026 after a 3.9% slump last year. Exports to the US account for about 75% of Canadian machinery gross output, making it one of the most exposed sectors to US import tariffs.

At least the industry benefits from fiscal measures which enhance existing tax allowances by enabling firms to deduct capital investment more rapidly and at a higher proportion of total cost.

We expect Chinese mechanical engineering output to increase by 6.1% in 2026, with the special purpose machinery segment growing 8.3%. In 2027 mechanical engineering production is forecast to rise 5.3%.

Demand from Chinese manufacturing sectors remains solid. Domestically the machines and engineering industry benefits from fiscal stimulus for advanced manufacturing and export-oriented sectors.

Mechanical engineering is additionally supported by government investment in strategic sectors such as high-tech, automation, and climate/energy, mainly benefitting the electrical machinery segment.

US tariffs remain a headwind for Chinese machinery and manufacturing exports. That said, global Chinese machinery exports benefit from the strength of pricing power and the ability of producers to either find new markets or reroute their products via other countries.

In the mid- and long-term, we expect Chinese annual mechanical engineering output to stabilise between 2.0% and 2.5%, as China is reaching the limits of its investment-driven growth model. A shift to a more service-oriented economy will reduce demand for capital goods.

Japanese mechanical engineering output is forecast to decline by 0.4% in 2026 before rebounding by 1.3% in 2027. Ongoing trade policy uncertainty still hampers capital expenditure growth in Japan and abroad. This is likely to weigh on sector activity over the next few quarters. A weakening global trade environment is a concern for a sector that heavily relies on foreign markets.

The new Japanese administration has approved a large supplementary budget focused on strategic industries and defence expansion, which should support medium-term investment in machinery. However, any further fiscal slippage risks triggering higher government bond yields, raising financing costs and limiting the effectiveness of fiscal support.

After contractions in 2024 and 2025 we expect mechanical engineering output in the EU and the UK combined to grow by 1% in 2026. The rebound remains modest due to a subdued manufacturing performance in the region, while the recovery of exports remains muted.

European mechanical engineering exports are highly dependent on the US market, meaning the sector is exposed to higher metals and aluminium import tariffs.

EU and UK machinery is potentially the most vulnerable European manufacturing sector to Chinese competition in external markets, as sales outside the region are a significant source of revenue for the industry. Over the past five years the EU global export market share in machinery has declined markedly, while China’s has increased.

Towards the end of 2026 sector growth should accelerate, and we expect machinery output in the region to increase by 1.9% in 2027, due to a rebound in manufacturing activity and expansion in defence and infrastructure-adjacent sectors.

Last year business uncertainty due to US tariffs have hampered investment decisions for machinery purchases, and exports to China and the US shrank by 8% year-on-year. Non-payments and insolvencies in the industry increased over the past two years.

We expect a modest 0.8% machines and engineering production rebound in 2026, followed by a 1.2% increase in 2027. Higher European defence spending and larger infrastructure investment in Germany triggered by fiscal stimulus should support the recovery. Also helpful will be tax breaks.

That said, the recovery of Germany’s economy remains slow for the time being. Demand from automotive as a key buyer industry is expected to decrease further. Deliveries to the US continue to suffer from high tariffs on the steel and aluminium components of machines, while competition from China is growing in many export markets. Therefore, we expect credit risk in the German machinery sector to remain elevated this year.

Download the full report in the related documents section below for a detailed analysis of the challenges, performance, and credit risks facing the metals and steel industry’s major markets throughout the world.

To explore to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.