Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

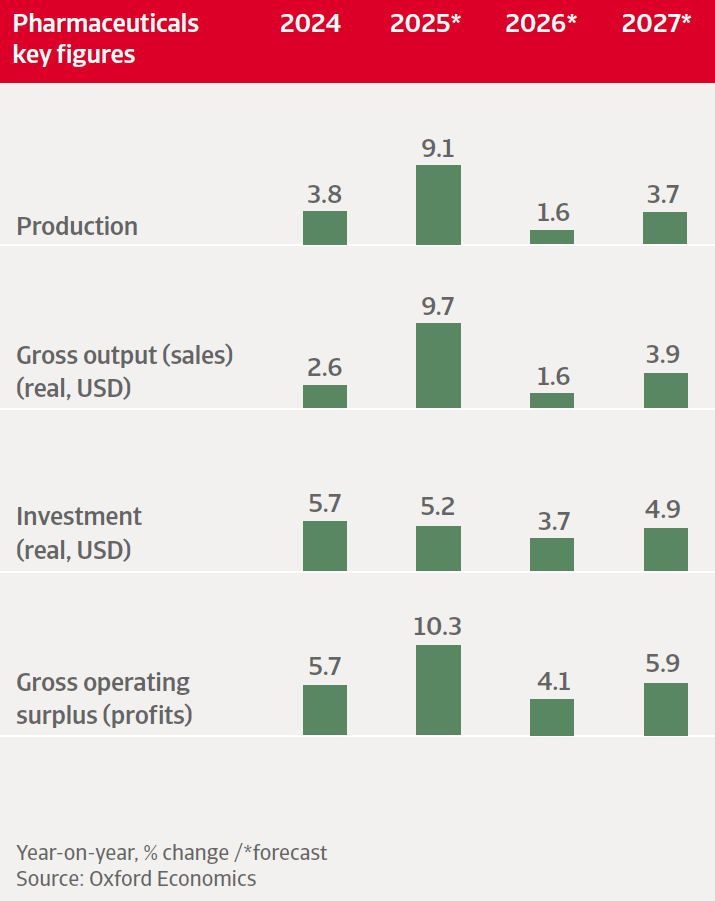

Global pharmaceutical production increased 9.1% in 2025, mainly due to front-loading activity in anticipation of US tariffs. In 2026 output growth is expected to slow down to 1.6%, as a retrenchment following last year’s surge will dampen production in H1 of 2026.

The impact of tariff threats has been limited so far, as the US has granted exemptions to most major pharmaceutical producers and tariff caps have been negotiated with countries. However, the downside risk of another tariff flare-up remains. In the coming years industrial policy will play a larger role throughout the global pharmaceuticals product value chain.

In general, the industry has robust equity, solvency and liquidity. Most pharmaceuticals and biotech businesses enjoy good access to external financing to help sustain high R&D costs.

Globally there is a shift towards premium and differentiated pharmaceutical products, including biologics, antibody-drug conjugates, and cell and gene therapies. We expect that Artificial Intelligence (AI) will increase productivity in the pharmaceutical sector in the coming years, mainly by supporting the preclinical phase and R&D in the production pipeline.

We expect US pharmaceuticals output growth to decelerate to 0.9% in 2026 after a strong 5.2% increase in 2025. In 2027 a 2.5% rebound is forecast.

The US administration has exempted generic drugs from import tariffs for the time being. Additionally, exemptions have been granted to individual drug companies and there are tariff caps on branded drugs imports. However, uncertainty remains, as Washington has repeatedly announced its intention to target medicine imports. Since September 2025, key pharmaceuticals have forged agreements with the Trump administration in exchange for tariff relief. They agreed to sell certain drugs and future medicines at lower prices under a so-called “most favoured nation” framework via TrumpRX.

It is expected that the Trump administration will decrease regulatory hurdles for domestic facility construction in order to incentivise reshoring to the US. This could further boost pharmaceuticals production in the US. However, high production costs could still make it more cost-effective for pharmaceuticals to be manufactured elsewhere.

“Despite major incentives, high production costs could hamper pharma reshoring to the US.”

Margins for branded pharmaceuticals are robust, leading to strong cash flow and credit profiles. Many US pharmaceutical companies seem financially strong or have ample liquidity sources in the financial markets.

While patented drugs will continue to dominate the market, there is growing competition as both generics and biosimilars increase their market share, driven by the loss of patent protections on established drugs.

The US government has taken steps to reduce the price of pharmaceuticals for consumers, which could erode businesses´ margins. Overall, the industry objects to those measures, arguing that they could lower innovation as businesses become discouraged from investing in R&D if returns on their investments are uncertain.

We expect Chinese pharmaceuticals production to grow by 6.6% in 2026 after a 3.6% increase in 2025. The sector’s short- and mid-term outlook remains benign.

The government has been successful in making the country attractive for pharmaceutical production and innovation, shifting away from producing generics and towards high-quality drugs and biopharmaceutical innovations. Measures include a series of capital investments, support of R&D, and policies to streamline approval processes and to align regulations to international standards.

Biologics and innovative drugs now account for roughly 40% of China’s development pipelines, with China contributing around 30% of global clinical trials (up from 5% ten years ago). Novel medicines are becoming the main growth engines, with domestic champions continuing to report strong innovation-drug revenue growth, even as legacy generic margins contract.

“Novel medicines are becoming the main growth engines in the Chinese pharma sector.”

The domestic market is highly price sensitive, as public procurement continues to suppress prices on mature drugs. In China most sales are still of generic drugs. State insurance covers most purchases, pooling demand from hospitals. In order to obtain coverage, producers have to lower prices to reach a large patient pool. The state’s volume-based procurement (VBP) programme is covering over 400 medicines cumulatively and driving average price cuts of 40%–60% on off-patent drugs, accelerating consolidation among small generic manufacturers.

Mid- and long-term domestic demand will be sustained by a growing middle class that can afford high value-added products. At the same time the population is ageing, which will spur demand for drugs related to chronic illnesses.

We expect Indian pharmaceuticals output to grow by 5.0% in 2026. Most businesses have strong balance sheets and good access to bank financing.

The government has introduced a National Pharmaceutical Policy (NPP), aimed at reducing drug costs and decreasing dependency on Chinese active pharmaceutical ingredient (API) imports. The policy offers financial incentives for the production of API, key starting materials and drug intermediates in India. As a result, India's API sector is expected to grow steadily.

India’s growing middle class and the increasing number of health insurance providers are enhancing access to medicines, which is expected to further stimulate domestic demand.

We expect pharmaceuticals output in Singapore to grow by 7.2% in 2026. Structurally, sector performance is supported by a business-friendly environment and proximity to key export markets in Asia. The credit risk situation of the industry is very good.

There will be significant investments in new manufacturing sites by major foreign pharma businesses in the coming years. However, Singapore’s lack of a trade agreement with the US leaves it vulnerable to a potential increase in US tariffs. Currently Singapore's exports to the US are subject to a 10% baseline tariff, but pharmaceutical products are exempted.

In Southeast Asia pharmaceuticals production and sales are projected to grow in 2026, led by Vietnam, where sector output is expected to increase by 8.2%. Key drivers include rising middle-class incomes, healthcare system development, and increasing investment from both domestic and foreign sources. Despite global trade and pricing pressures, the credit risk of pharmaceuticals in Southeast Asia remains favourable with stable macroeconomic conditions.

“Better healthcare systems and rising incomes drive pharma growth in Southeast Asia.”

After sharply increasing by 21.6% in 2025, pharmaceuticals production in the Eurozone is expected to contract temporarily in 2026, by 3.7%. The surge seen last year was due to front-loading triggered by massive US tariff threats, in particular benefitting Ireland.

For the time being US tariffs on EU pharma goods remain capped at 15%, and there are exemptions granted to European pharma companies that have agreed to increase production in the US. This limits the impact of tariffs on the sector in the EU. However, moving manufacturing to the US requires substantial capital investment and operational restructuring, posing challenges for smaller companies with limited resources.

The UK has secured a zero percent tariff on pharmaceutical exports to the US, in exchange for a significant concession on medicine pricing. The agreement with the US has removed a major external risk to pharma exports and is boosting confidence in export-based manufacturing.

The demand outlook for pharmaceuticals in Europe is solid in both the mid- and long-term. Pharmaceutical producers and wholesalers will benefit from the region’s ageing population.

Most of the individual markets in Europe are highly regulated, and many feature constraints that could impact pharma profits. There is permanent pressure from national health authorities to lower prices of drugs and medicines.

For the most part, financial indicators in the industry are strong, but some SMEs could face financing challenges. This is due to high R&D costs, competition from India and China, and difficulty accessing financing at competitive interest rates.

European businesses face competitive disadvantages as more pharmaceutical businesses invest in the US and China, at the expense of investments in Europe over the coming years. Despite well-established manufacturing facilities, secure supply chains and high production standards, the EU is facing gradually decreasing competitiveness in innovation. This is due to slower clinical trial setup times, weakening its ability to develop and produce new drugs early, in addition to less favourable regulatory and funding environments and smaller patient pools compared to the US and China.

“The EU is facing gradually decreasing competitiveness in pharma innovation.”

Download the full report in the related documents section below for a detailed analysis of the challenges, performance, and credit risks facing the pharmaceuticals industry’s major markets throughout the world.

To explore to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.