Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

Brazil

Brazil

Portugal

Portugal

Spain

Spain

アイルランド

アイルランド

アラブ首長国連邦

アラブ首長国連邦

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

スロベニア

スロベニア

チェコ共和国

チェコ共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

リトアニア

リトアニア

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

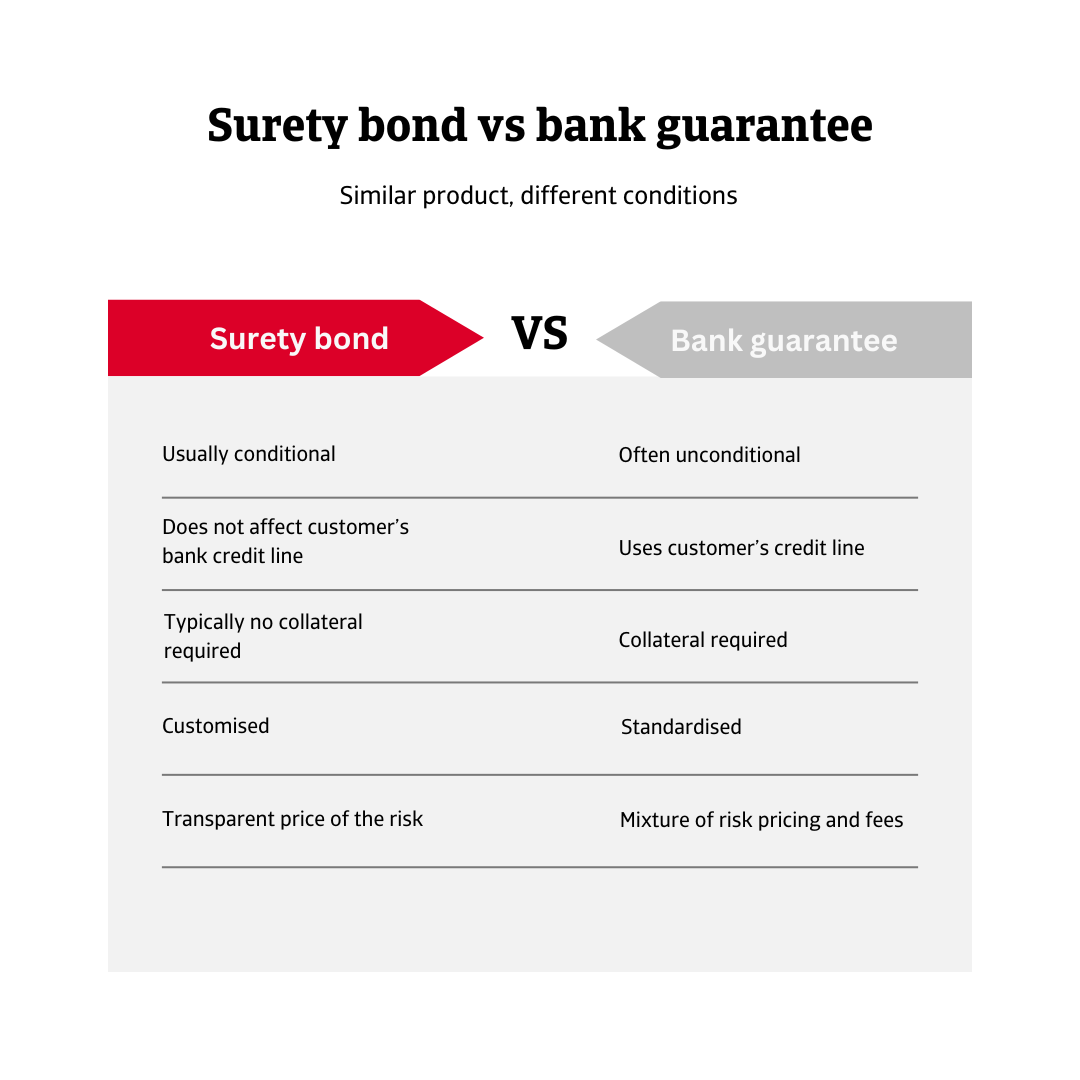

In today’s global economy, trust and reliability are essential to every business relationship. When entering a commercial agreement, it’s vital to ensure that contractual obligations are met. Any breach, regardless of the cause, can damage a company’s financial health and even threaten its future. To reduce this risk, businesses use financial instruments that offer an extra layer of protection: surety insurance and bank guarantees.

Both are widely accepted by public and private organisations as valid forms of financial assurance. While they serve similar purposes, they differ significantly in structure, cost and impact on financial flexibility.

A bank guarantee is a contract where a financial institution agrees to cover a client’s obligations if they fail to meet them. Before issuing the guarantee, the bank assesses the client’s creditworthiness and may ask for collateral or asset blocking.

A surety bond is an alternative to bank guarantee, provided by insurers such as Atradius. It offers the same level of protection to the beneficiary, but with several operational and financial advantages.

.2025-11-07-13-51-55.png)

A surety bond is a conditional commitment issued by the insurance company, guaranteeing that the principal will fulfil a defined obligation. Due to its conditionality, the bond only activates if the principal fails to perform on this obligation.

In contrast, a bank guarantee is often unconditional, meaning the bank may be required to pay upon demand, regardless of whether the principal has defaulted on an obligation.

Considering guarantees as contingent liabilities, banks count them against a customer’s overall credit lines, which can limit access to new financing and reduce flexibility for strategic investments or operational needs.

Capacity obtained from a surety comes on top and does not interfere with credit capacity obtained from a bank.

Insurers issuing surety bonds typically do not require asset-based collateral, allowing companies to retain full access to their financial resources and maintain liquidity. Banks, on the other hand, often require taking charges on assets as collateral before issuing a guarantee, following a thorough credit assessment.

Unlike bank guarantees, which are typically standardised and offer limited flexibility, surety bonds can be tailored to meet the specific requirements of a project or contract. This adaptability makes them especially valuable in complex or specialised transactions.

Surety bonds typically involve a single, transparent premium based on risk assessment, often with annual reviews for ongoing coverage. Bank guarantees typically blend risk remuneration with multiple fees.

For companies in sectors that require frequent guarantees (such as construction, renewable energy, international trade or public procurement), surety bond offers a flexible and cost-effective solution. It helps businesses optimise resources, access financing, respond quickly to guarantee demands and avoid unnecessary administrative overhead.

While both instruments protect contractual relationships, surety insurance stands out as a modern, efficient alternative to traditional bank guarantees. It enables companies to meet obligations without compromising liquidity or credit capacity, a strategic advantage in today’s competitive global markets.

To explore how to strengthen your own risk management strategy, get in touch with us and see how we can help you stay ahead.