Atradius Atrium

保険契約情報、与信限度額申請ツール、インサイトに直接アクセスできます。

日本

日本

アイルランド

アイルランド

イギリス王国

イギリス王国

イタリア

イタリア

インド

インド

オーストラリア

オーストラリア

オーストリア

オーストリア

オランダ

オランダ

カナダ

カナダ

ギリシャ

ギリシャ

シンガポール

シンガポール

スイス

スイス

スウェーデン

スウェーデン

スロバキア

スロバキア

チェコ語共和国

チェコ語共和国

デンマーク

デンマーク

ドイツ

ドイツ

トルコ

トルコ

ニュージーランド

ニュージーランド

ノルウェー

ノルウェー

ハンガリー

ハンガリー

フィンランド

フィンランド

フランス

フランス

ブルガリア

ブルガリア

ベルギー

ベルギー

ポーランド

ポーランド

メキシコ

メキシコ

ルーマニア

ルーマニア

香港SAR

香港SAR

中国

日本

中国

日本

米国

米国

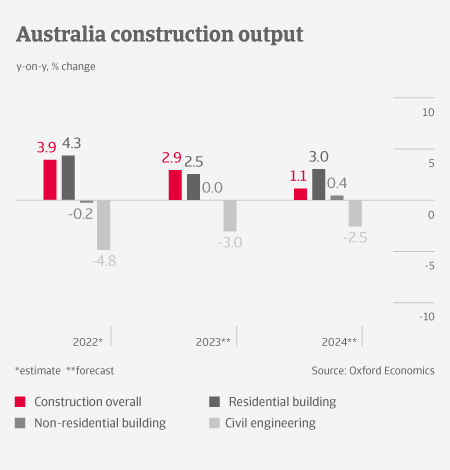

In 2023, Australian construction output is expected to slow somewhat, to about 3%. Residential building is impacted by elevated inflation and increasing interest rates, which have led to a deterioration of property prices, while construction costs have surged.

Margins of builders and subcontractors were severely impacted in the Financial Year 2022 (1 July 2021-30 June 2022) due to sharply increased costs for construction materials, coupled with fixed price contracting. Since 2022, most new contracts contain escalation clauses, which enable construction businesses to pass on a large part of increased input prices.

That said, all construction subsectors still suffer from ongoing labour and material shortages. This is extending build times and costs, threatening the viability of future projects. Supply shortages lead to inefficiencies and problems with scheduling. As a result, construction businesses are facing cash flow issues. Skilled labour shortage in Australian is one of the key challenges for the sector, leading to soaring labour costs, which puts pressure on margins.

That said, all construction subsectors still suffer from ongoing labour and material shortages. This is extending build times and costs, threatening the viability of future projects. Supply shortages lead to inefficiencies and problems with scheduling. As a result, construction businesses are facing cash flow issues. Skilled labour shortage in Australian is one of the key challenges for the sector, leading to soaring labour costs, which puts pressure on margins.

Payments in the Australian construction industry take about 60-90 days on average, and the number of payment delays is high. However, the majority of these are of small amount, and are finally settled.

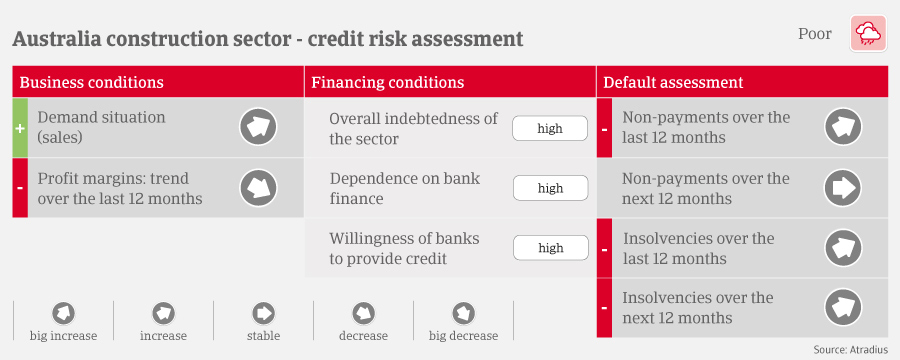

Construction insolvencies increased sharply in 2022, as builders struggled with high prices for key materials, while many had taken on too many projects that were no longer profitable, causing them to go bust. However, this increase was from a very low level, because during the pandemic several forms of government support led to sharp decreases in 2020 and 2021. We expect further rising construction business failures in 2023 because cash flow issues persist for many construction companies and market conditions remain volatile. Therefore, we still assess the credit risk situation of the industry as “Poor”.